Is M1 Finance Worth It for Long‑Term Investors in 2026?

M1 Finance has evolved significantly since its 2015 launch, positioning itself in 2026 as what the company calls a “Finance Super App.” The platform combines brokerage accounts, high yield cash account services, margin loans, and limited cryptocurrency exposure under one roof. At its core sits the visual “Pie” system—an intuitive way to structure your investment portfolio as customizable slices representing target allocations to stocks, exchange traded funds, or nested sub-Pies.

This m1 finance review targets long-term, mostly passive investors—especially beginners to intermediates aged 25-45 who appreciate automation tools and clean visual dashboards over spreadsheets and manual trading. If that sounds like you, keep reading.

So, is M1 Finance any good? Here’s the quick verdict: it excels for disciplined, long-term investing with its automated features and fractional shares capabilities. However, it’s a poor fit for active traders, options enthusiasts, or anyone requiring mutual funds and full-service advisory.

Key 2026 facts worth knowing: there’s a $3 monthly fee for investment accounts under $10,000 in total assets (waived once you hit that threshold), zero trading fees on stock and ETF trades, access to 6,000+ securities, and support for fractional shares down to $1 minimum investments. The platform also offers limited crypto like Bitcoin and Ethereum.

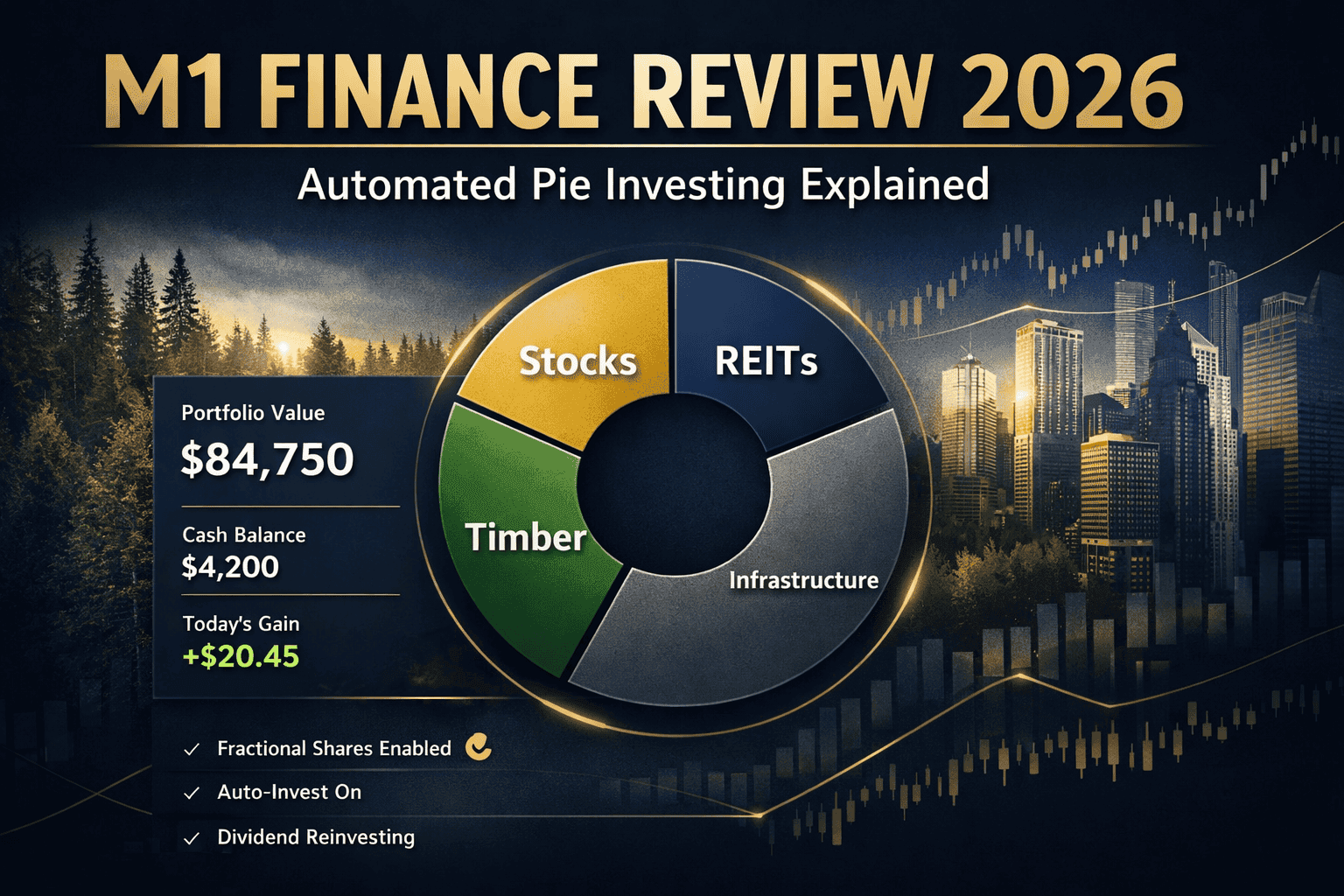

Throughout this review, Witty Investor will walk you through a concrete “Forestry & Real-Assets” model portfolio—a strategy particularly relevant for readers concerned about inflation protection and real-asset diversification.

Quick pros and cons:

- Pros: Zero commissions, powerful automation, fractional shares, intuitive Pie system, integrated banking

- Cons: Limited trading windows, no options or mutual funds, basic research tools, monthly fee for smaller accounts

Our Take at Witty Investor

M1 Finance occupies a unique middle ground between a self directed brokerage accounts platform and robo advisor automation. You get the control of picking individual stocks and ETFs while benefiting from automated investing strategies that typically require expensive advisory services.

It’s important to clarify: M1 is not a traditional robo advisor. There’s no human financial advice, no automated tax-loss harvesting, and no comprehensive goal-planning tools. Instead, you get model portfolios (“Pies”) and dynamic rebalancing that handles the mechanical work of keeping your portfolio aligned with your targets.

The $3 monthly fee in 2026 applies to accounts below $10,000. New accounts receive a 90-day grace period before this fee kicks in. Once your cash balance plus investments crosses $10,000 even briefly during a billing cycle, the fee disappears. For sophisticated wealth building on a budget, this structure rewards consistency.

At Witty Investor, we find M1 particularly attractive for buy-and-hold portfolios incorporating thematic allocations—like forestry, infrastructure, and REITs. The Pie system makes implementing these strategies remarkably straightforward.

- Best for: Long-term investors, set-and-forget portfolio builders, those comfortable with DIY decisions

- Not ideal for: Day traders, options strategists, investors requiring mutual funds or human advisors

Where M1 Finance Shines

This section focuses on the strengths most relevant to investors in 2026.

The Pie system remains M1’s standout feature. Each portfolio appears as a visual circle divided into slices—up to 100 per Pie. You can combine individual stocks, ETFs, and even crypto into a single, easily monitored view. Sub-Pies allow nesting strategies within strategies, perfect for maintaining separate allocations to domestic equities, international funds participating in global markets, and real assets.

M1’s automation tools deserve special attention. Enable Auto-Invest, schedule recurring deposits, and watch as new money flows automatically into underweight slices during the next trading window. This dynamic rebalancing means your $200 monthly contribution might buy 60% into an underweight timber REIT and 40% into lagging infrastructure—all without manual intervention.

Fractional shares fundamentally change what’s possible with small contributions. Want exposure to $300+ stocks like Berkshire Hathaway Class B with just $50? No problem. This precision matters for users who want to start investing with modest amounts while maintaining exact target allocations.

Portfolio customization options are extensive. Browse 80+ pre-built Expert Model Portfolios covering everything from 60/40 allocations to socially responsible investing themes. Or build completely custom Pies—like the Forestry/Real-Asset strategy we’ll detail shortly.

The integrated high yield cash account yields approximately 4% APY in early 2026, with FDIC insured coverage up to $3.75 million through partner bank sweep program banks. Smart transfers automate money movement between checking and investing based on rules you define.

Key strengths:

- Zero commission on stock and ETF trades

- Fractional shares enable precise diversification from $1

- Visual Pie system simplifies complex portfolios

- Auto-Invest removes emotional decision-making

- Mobile-first design with full feature parity

- Integrated banking with competitive cash yields

Where M1 Finance Falls Short

The same features that help long-term investors can frustrate experienced investors seeking active trading capabilities. M1’s deliberate design choices create real limitations worth understanding.

Trading windows are restricted: orders execute during a primary window at 9:30 a.m. Eastern. A secondary 3:00 p.m. window becomes available for accounts exceeding $25,000 in equity or M1 Plus subscribers ($95/year). There’s no intraday trading, no after-hours execution, and no real-time orders. Your carefully planned entry could slip 0.5-1% during volatile opens.

The platform excludes options trading entirely, along with mutual funds and individual bonds. Income strategies like covered calls (which can yield 5-10% premiums) or bond ladders simply aren’t possible here. If your investing strategy depends on these instruments, M1 isn’t your platform.

Research tools remain basic compared to a traditional broker like Fidelity or Schwab. You’ll find simple screeners, profile pages with P/E ratios, and charts powered by Quotemedia—but no backtesting, algorithmic scanners, or deep analyst reports. Market research must happen elsewhere.

Fee pain points exist for smaller accounts. That $3 monthly fee equals $36 annually—fine for $15,000+ accounts but expensive as a percentage for a $3,000 portfolio. Account closure fees and other fees add up: $100 for outgoing ACATS transfers, $100 for IRA closures. An inactive $40 account triggers a $50 inactivity fee after 90 days, effectively wiping it out. Regulatory fees and ADR fees may also apply to certain securities.

M1 offers no tax-loss harvesting and no human financial advisors. This platform assumes you’re comfortable making your own decisions.

Drawbacks checklist:

- You want to day trade or need real-time execution

- You insist on mutual funds or options strategies

- You require personalized financial advice

- You’re starting with under $500 and uncertain about consistency

- You need advanced research and backtesting tools

M1 Finance at a Glance (2026 Snapshot)

Here’s your quick-reference summary for M1 Finance in 2026.

Account Minimums:

- Taxable brokerage: $100

- Retirement accounts (Traditional, Roth, SEP IRAs): $500

- Custodial accounts: Available with standard minimums

- Trust accounts: $5,000 minimum

- Cash account: $100

Tradable Assets:

- 6,000+ U.S. stocks and ETFs

- Limited crypto (Bitcoin, Ethereum, Litecoin)

- USD pairs only—no crypto-to-crypto trading

- No mutual funds, options, or most OTC stocks

Core Pricing:

- $0 trading commissions on stocks/ETFs

- $3/month platform fee (waived at ≥$10,000)

- Margin rates: 6-8% (tiered, $2,000 minimum to access margin accounts)

- Cash account APY: ~4% (variable)

Key Protections:

- SIPC insurance: Up to $500,000 ($250,000 cash)

- FDIC insurance on swept cash: Up to $3.75M+ via sweep program partner banks

Specs at a glance:

- Account types: Individual, Joint, IRA (Traditional/Roth/SEP), Custodial, Trust, Cash

- Trading windows: 9:30 a.m. ET primary; 3:00 p.m. ET secondary (with qualifications)

- No management fees beyond platform fee

- No charge commission on standard trades

Account Types, Sign‑Up, and Platform Experience

Opening an M1 account takes roughly 10 minutes with approval typically within one business day. The process is entirely online—no branch visits required.

Supported account types:

- Individual and joint taxable brokerage

- Traditional IRA, Roth IRA, SEP IRA

- Custodial accounts (UGMA/UTMA)

- Trust accounts

- High-yield cash accounts

- Crypto investing (integrated)

Onboarding steps:

- Visit M1’s website or download the app; create login credentials

- Complete identity verification (SSN, address, employment)

- Answer risk tolerance and experience questions

- Choose your account type based on goals

- Link your bank via Plaid for instant verification

- Fund via ACH (4-5 days settlement for withdrawals; instant for deposits)

- Build or import a Pie and enable Auto-Invest

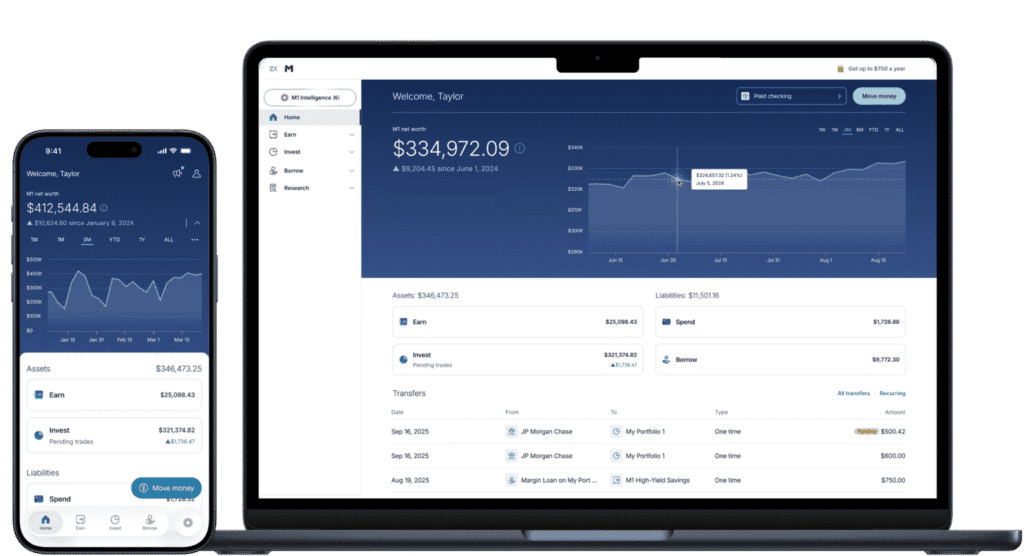

The desktop experience centers on a clean dashboard with your main Pie visualization, performance charts, and activity log. The Research tab offers basic screeners. The mobile app (Android and iOS) mirrors desktop functionality completely—Pie editing, alerts, deposit scheduling, and dividend tracking all work identically on phone.

External transfers via ACATS are supported, though outgoing transfers incur that $100 fee. Plan your moves accordingly.

Portfolio Construction on M1: Pies, Model Portfolios & Forestry / Real‑Asset Strategy

Pies function as M1’s core portfolio engine. Each Pie contains slices—individual securities or sub-Pies—with target percentages you define. The platform then works to maintain those targets through automation.

M1 offers 80+ Expert/Model Portfolios covering broad range allocations (60/40 stock-bond), dividend strategies, responsible investing themes, and factor-based tilts. These provide excellent starting points for beginners.

The real power emerges through customization. Blend multiple Model Pies, add individual stocks, adjust weights, and create different configurations for taxable versus retirement accounts. This flexibility enables strategies that most robo advisors simply don’t allow.

Witty Investor’s Forestry & Real-Asset Model Pie

Real assets matter for long term investing. Timber, infrastructure, and commodities historically deliver low correlations to equities—studies show real-asset tilts can reduce portfolio volatility by 10-20% during high-inflation periods like 2022. Timber returns have averaged 8-12% annually over decades, hedging inflation through physical asset appreciation.

Here’s our suggested allocation framework:

- Global Listed Timber & Forestry (25-35%): U.S. timber REITs and global forestry companies managing millions of acres provide direct timberland exposure

- Listed Infrastructure ETFs (20-30%): Toll roads, utilities, pipelines, and airports typically yield 3.5-4.5% with global diversification

- Diversified REIT ETFs (15-25%): Industrial, logistics, and residential properties benefiting from e-commerce growth

- Commodity/Natural Resource ETFs (15-25%): Metals, agriculture, and energy producers via low-cost funds

- Broad Market Equity Anchor (5-10%): Global or total market ETF to maintain correlation with overall markets

Implementation on M1:

- Use the Research tab to locate timber, infrastructure, REIT, and commodity ETFs

- Add each as a slice with target weights matching the ranges above

- Save as a custom “Forestry & Real Assets” Pie

- Consider allocating 20-40% of your overall portfolio to this Pie, with remaining funds in broad global equity and bond Pies

This model suits investors concerned about long-term inflation, those seeking diversification beyond traditional stocks and bonds, and users comfortable with sector concentration risk. It’s particularly relevant for American foresters and those in applied sciences fields who understand timber and resource markets.

Portfolio Management, Automation & Dynamic Rebalancing

M1 executes trades around your target Pie weights rather than processing individual orders like other brokerage platforms. This approach fundamentally changes how you interact with your money.

Auto-Invest: Once enabled, deposits exceeding your set cash threshold automatically flow into underweight slices during the next trading window. Set it and forget it.

Dynamic Rebalancing: New contributions and dividends funnel into slices below their targets, reducing the need to sell overweight positions—and the taxable events that come with them.

One-Click Manual Rebalancing: Need to realign quickly? Hit “Rebalance” and M1 sells overweight slices while buying underweight ones. In taxable accounts, this triggers capital gains, so use sparingly.

Trading windows aggregate all your orders into single daily executions. This limits timing precision but simplifies life for long-term investors who shouldn’t care about intraday moves anyway.

Fractional shares keep portfolios remarkably close to targets even with $50 monthly deposits. A $300 REIT ETF stays at exactly 15% allocation despite daily price swings—precision that whole-share brokers simply can’t match.

Key automation behaviors:

- New deposits invest into underweight slices first

- Dividends reinvest according to current targets

- Tax-efficient sell order prioritizes lots with lowest tax impact

- All orders batch into morning (and optional afternoon) windows

- No full tax-loss harvesting—this is not managed for you

Cash Management, Margin & “Borrow” Features

M1’s positioning as a “Finance Super App” means investing, cash management, and borrowing live under one roof.

The high yield cash account offers approximately 4% APY in 2026, with FDIC insurance coverage up to $3.75 million through partner bank networks. Uninvested cash earns this interest rate automatically. There’s no minimum balance requirement, and money moves seamlessly between cash and investing Pies.

Smart Transfers automate rule-based money movement. Examples: “Keep checking above $2,000, sweep program leave excess into investing.” Or: “Refill emergency fund before sending money to my Forestry Pie.” This helps maintain your customer profile level of liquidity.

Margin (“Borrow”) basics:

- Minimum $2,000 invested to qualify

- Borrow up to ~50% of eligible portfolio value

- Margin rates typically 6-8%—lower than many legacy brokers

- Interest compounds; risk increases with leverage

Strategic uses include short-term liquidity without selling investments, or tax optimization by drawing margin loans instead of realizing gains on appreciated positions. This mirrors “buy, borrow, die” tactics discussed in sophisticated wealth planning.

Safe-use guidelines from Witty Investor:

- Never borrow more than 25% of portfolio value

- Avoid margin on volatile real-asset and commodity holdings

- Maintain cash buffer for potential margin calls

- Remember: no margin in retirement or custodial accounts

- Investing involves risk—leverage amplifies both gains and losses

Fees, Costs & How M1 Makes Money

M1 Finance charges $0 commissions on self-directed stock and ETF trades. However, account fees exist and matter for certain users.

Investor-facing fees:

- $3/month platform fee for accounts under $10,000 (waived at ≥$10,000 after 90-day intro period)

- $50 inactivity fee for dormant accounts with balances ≤$50 after 90+ days

- $100 outgoing ACATS transfer fee (full transfers)

- $100 IRA closure fees

- Variable margin interest (tiered, approximately 6-8%)

- Underlying ETF expense ratios (typically 0-0.10% for index funds)

How M1 makes money:

- Payment for order flow (PFOF)

- Interest spread on cash holdings

- Securities lending

- Margin interest income

- Debit/credit card option interchange fees

Cost comparison scenario: A $5,000 account pays $36/year ($3 × 12 months). A robo advisor charging 0.25% AUM would cost $12.50/year on the same balance. M1 appears expensive here.

At $15,000, M1’s flat $36 fee equals 0.24%—suddenly competitive. Above $20,000, M1 becomes meaningfully cheaper than percentage-based robos.

For funds participating in M1’s ecosystem at scale, costs compare favorably to both traditional broker platforms and robo advisors. The company founded by Brian Barnes has built a model that rewards account growth.

Investment Selection, Research Tools & Education

M1’s investment universe spans 6,000+ U.S. stocks and exchange traded funds, plus a limited but growing crypto lineup. Notably absent: mutual funds, options, and most OTC/penny stocks.

For real-asset enthusiasts, the securities available support our Forestry model nicely—listed timber REITs, global resource companies, infrastructure ETFs, and commodity-linked funds all trade on M1’s platform.

The Research tab provides basic functionality: screeners by sector, market cap, dividend yield, and other fundamentals. Profile pages show key metrics. Performance charts track historical returns. But you won’t find backtesting, institutional-grade analytics, or deep company reports.

M1’s educational content focuses on a blog, videos, and newsletters covering general investing topics—portfolio basics, retirement planning, market commentary. There are no interactive planning tools or personalized guidance.

Research strengths and gaps:

- Adequate for identifying well-known ETFs and blue chips

- Basic screening for dividend yield, sector, market cap

- Limited fundamental data compared to Fidelity, Schwab

- No analyst ratings or earnings estimates

- No water quality-style deep dives on individual securities

Witty Investor serves as a complementary resource for deeper analysis on strategies like forestry allocations and diversified portfolio design. Use both.

Safety, Security & Customer Support

M1 Finance operates as a SEC-registered broker-dealer and FINRA member. Your investment accounts receive standard regulatory protections.

Investor protections explained:

- SIPC insurance covers up to $500,000 per customer (including $250,000 cash) against broker failure—not market losses

- FDIC insurance on swept cash accounts reaches multi-million coverage through sweep program banks partnership

- Your securities exist separately from M1’s company finances

Digital security features:

- Two-factor authentication required

- Device verification for new logins

- Strong encryption standards

- Account-level security alerts

Customer service operates via email, web form, and phone during weekday hours (approximately 9 a.m.-4 p.m. Eastern, excluding market holidays). Response times typically run 1-2 business days, with potential delays during high-volume market events.

What “safe” means:

- Regulated by SEC and FINRA

- SIPC and FDIC insurance in place

- Technical controls meet industry standards

- No 24/7 support or human advisory available

Who Should Use M1 Finance – and Who Should Avoid It?

Ideal M1 users:

- Investors focused on 5-20+ year horizons with rules-based portfolios

- People who appreciate visual allocation tools and automated rebalancing

- Those interested in thematic strategies like forestry and infrastructure without complex spreadsheets

- Mobile-first users comfortable managing money digitally

- Investors seeking a bachelor’s degree level of financial understanding who want execution simplicity

- Customers building through consistent contributions rather than lump-sum timing

Look elsewhere if:

- You require real-time execution and intraday trading

- Your strategy depends on options, mutual funds, or active bond-laddering

- You want human advisors guiding every decision

- You need comprehensive withdrawal planning for retirement income

- Trading frequency matters more than automation

Concrete example: A 30-year-old professional building a diversified retirement portfolio—with a 25% Forestry/Real-Asset sleeve alongside global equities—fits M1 perfectly. A retiree needing active withdrawal strategies, bond ladders, and regular advisor check-ins should consider full-service alternatives.

How to Get Started with M1 Finance (Step‑by‑Step)

Opening your account:

- Create account: Visit M1’s site or download the app; enter email and create password

- Verify identity: Complete KYC (name, address, SSN, employment, investing experience)

- Choose account type: Select taxable brokerage, Roth IRA, or another option based on goals

- Link bank: Connect via Plaid for instant verification; decide on initial deposit (minimum $100 for brokerage)

- Build your Pie: Start with an Expert/Model Pie or construct custom allocations (e.g., core global equity plus Witty Investor’s Forestry Pie as satellite)

- Enable automation: Toggle Auto-Invest on, schedule recurring deposits matching your cash flow

- Review annually: Reassess allocations after major life changes; resist frequent tinkering

Before committing, align your M1 setup with broader financial products and goals—retirement timelines, emergency funds, risk tolerance, and other investment priorities. The platform rewards consistency over activity through hands on testing of your patience.

Bottom Line: Our Verdict on M1 Finance in 2026

M1 Finance delivers on its core promise: low-cost automation for disciplined, long-term investors. The Pie system makes implementing sophisticated strategies—including real-asset allocations like our Forestry model—remarkably accessible. For users willing to handle their own research and decision-making, M1 provides institutional-quality execution mechanics without advisory costs.

That said, M1 isn’t a complete list of everything investors might need. It lacks the trading flexibility, research depth, and advisory services that some portfolios require. Smaller accounts face meaningful fees until reaching $10,000.

Reasons to open an M1 account:

- You want automated, long-term portfolio management

- Fractional shares and zero commissions matter to you

- You’re comfortable with DIY decision-making

- Integrated banking and competitive cash yields appeal

- You want to implement thematic strategies like forestry/real assets easily

Reasons to skip it:

- You need real-time trading or options

- Mutual funds are central to your strategy

- You require human financial advisory

- Your account will stay under $5,000 indefinitely

We recommend comparing M1 with at least one other brokerage and one traditional robo advisor before committing. Use Witty Investor’s educational resources to refine your portfolio design—whether that’s a Forestry Pie, dividend strategy, or simple three-fund approach. The best platform is the one that matches your actual investing behavior.

Keep Your Investing Edge Sharp: