(A brutally honest guide for anyone who’s ever panic-sold, FOMO-bought, or checked their portfolio 17 times during lunch.)

Your brain is an incredible piece of survival hardware. Unfortunately, it was built for sabertooth tigers… not stock tickers.

And the financial system? It LOVES that your brain is still basically a caveman with Wi-Fi.

Here’s the uncomfortable truth about why most people suck at money: it’s not because they’re stupid, lazy, or unlucky. It’s because their psychology is actively working against them every single day. The same mental shortcuts that kept your ancestors alive on the savanna are now bankrupting you in broad daylight.

Today we’re diving into the 7 psychological sins that explain why most people suck at money — even smart people, even rich people, even that Reddit guy with the “Trust Me, Bro” stock tips. These aren’t just abstract concepts from dusty academic journals. These are the actual cognitive biases that Daniel Kahneman won a Nobel Prize for documenting, and they’re costing you a fortune.

If you can recognize these sins in yourself, you’ll stop sabotaging your wealth and start building it. Because understanding why most people suck at money is the first step toward not being one of them.

Sin #1 — Fear: The Market Monster Under Your Bed

Fear is the primary reason why most people suck at money, and it manifests in ways that seem completely rational in the moment but are financially catastrophic over time.

Fear makes people:

- Sell low (usually at the exact worst moment)

- Buy high (because “safe” feels better when everyone else is already in)

- Hoard cash earning 0.01% while inflation eats their lunch

- Avoid investing entirely, preferring the “safety” of guaranteed losses

- Believe every YouTube video titled “CRASH ALERT: WATCH NOW!”

- Check their portfolio during market dips like they’re watching a horror movie

Here’s what the research shows: According to studies on investor behavior and market timing, the average investor dramatically underperforms the market itself — not because of bad stock picks, but because of terrible timing driven by fear.

Fear feels logical in the moment… but financially, it’s duct-taping yourself to a sinking ship while the rescue boat is literally right there.

The amygdala — your brain’s fear center — doesn’t understand that a 20% market correction is normal. It just sees RED NUMBERS and screams “DANGER!” like you’re about to be eaten. This is precisely why most people suck at money: they let their lizard brain drive their financial decisions.

What to do instead

- Automate investing so your emotions don’t get a vote in the process

- Zoom out to the 10–20 year chart (where fear looks ridiculous in hindsight)

- Build a written plan BEFORE you invest — not during a crash when your judgment is compromised

- Quantify your fears by running actual numbers on worst-case scenarios

- Pre-commit to buying more when markets drop (because that’s literally when things are on sale)

Sin #2 — Greed: The ‘I Need 10% a Week’ Syndrome

If fear explains why most people suck at money on the downside, greed explains why they suck at it on the upside.

Greed tells you:

“Why settle for 8% a year when that guy on TikTok is making 400% flipping options?”

Greed blinds you to risk — and turns you into a lottery-ticket investor who mistakes a bull market for genius. It’s why people who made money in 2021 by throwing darts at a crypto board convinced themselves they were financial prodigies… right before losing 70% in 2022.

The psychological mechanism here is called “overoptimism bias,” and it’s been studied extensively. People systematically overestimate their chances of positive outcomes while underestimating risks. This is why most people suck at money even when markets are going up — they’re so greedy they can’t see the cliff edge.

WI Translation

If your plan relies on luck, timing, or vibes… it’s not a plan. It’s a prayer with a brokerage account.

What to do instead

- Avoid get-rich-yesterday strategies (they’re get-poor-tomorrow strategies in disguise)

- Stick to repeatable systems that work in multiple market conditions

- Focus on long-term wealth, not dopamine hits that feel like validation

- Calculate realistic returns based on historical data, not YouTube thumbnails

- Remember: Greed is just fear wearing a gold chain

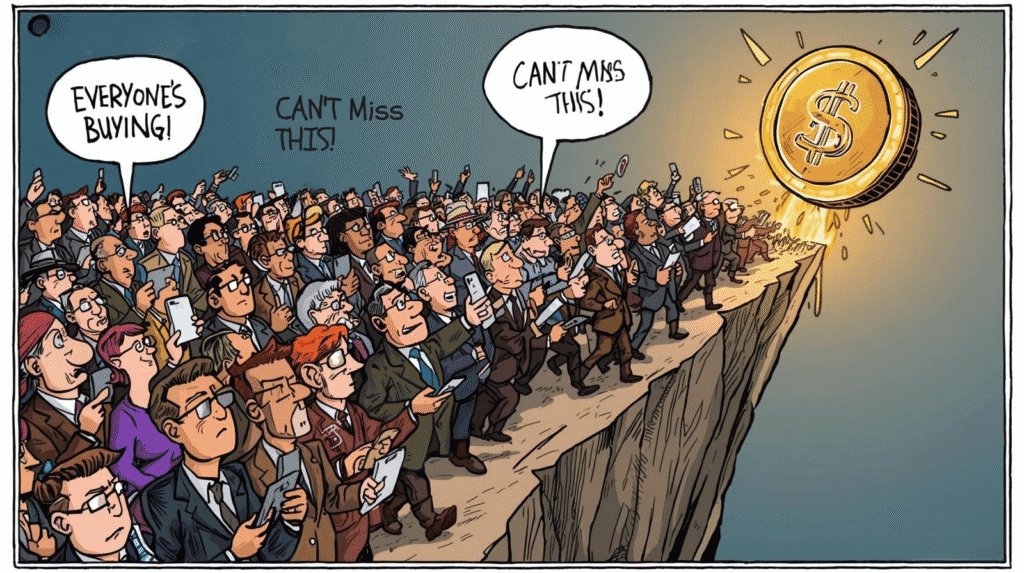

Sin #3 — FOMO: Fear of Missing Opportunities (AKA “The Neighbor Bought a Rental… Should I?”)

FOMO — Fear of Missing Out — is one of the top reasons why most people suck at money in the modern era. It didn’t exist when your grandparents were investing because they couldn’t see everyone else’s wins in real-time.

Now? You’re bombarded with:

- Your coworker’s Tesla stock gains

- Your cousin’s crypto “moon shot”

- That influencer’s real estate empire

- Reddit threads about 1000% returns

FOMO makes people chase:

- Meme stocks at the peak

- Crypto during bubble mania

- Real estate in bidding wars

- “This time it’s different” narratives

- Anything that’s already run up 500%

You’re not investing — you’re stampeding. And stampedes end badly.

The research on herd behavior in financial markets shows that investors consistently pile into assets after they’ve already appreciated significantly. This is exactly why most people suck at money: they buy high because everyone else is buying, then sell low when the crowd panics.

What to do instead

- Create an investment thesis BEFORE you buy (if you can’t write it down, you don’t have one)

- Treat hype like an alarm, not an invitation

- Weirdly enough… run the math on what returns you’d actually need

- Ask yourself: “Would I buy this if no one was talking about it?”

- Implement a waiting period before chasing anything trending

Sin #4 — Overconfidence: The ‘I’m Basically Warren Buffett’ Illusion

This sin hits men hardest. (Sorry, fellas — the data backs me up.)

Studies from behavioral finance researchers like Terrance Odean have shown that men trade 45% more frequently than women… and earn 1.4% less annual returns because of it. Male overconfidence literally costs money.

Signs you’re afflicted:

- You think you can pick the exact top and bottom

- You YOLO into a stock because the “chart looks right”

- You assume the market cares about your opinion

- You’ve used the phrase “easy money” unironically

- You think you’re smarter than professional fund managers (who also underperform)

This is why most people suck at money even when they’re intelligent: they confuse general intelligence with financial expertise. You can be a brilliant engineer, doctor, or lawyer and still be terrible at investing because overconfidence tricks you into thinking your skills transfer.

The Dunning-Kruger effect is alive and well in investing: people with the least experience tend to have the most confidence. Actual expert investors? They’re scared all the time because they know what they don’t know.

What to do instead

- Use checklists (pilots use them; so should you)

- Ask: “What would prove me wrong?” before making any investment

- Accept that markets are smarter than you (they’re the collective wisdom of millions)

- Track your predictions and review them honestly

- Seek disconfirming evidence actively

Sin #5 — Loss Aversion: Losing $100 Hurts More Than Gaining $100 Feels Good

Loss aversion is the psychological phenomenon discovered by Kahneman and Tversky that explains why most people suck at money even when they know better.

Psychologically, losses hurt about 2-2.5 times more than equivalent gains feel good. Your brain is wired asymmetrically, which means you’re not making rational cost-benefit analyses — you’re making emotional survival calculations.

Loss aversion is why people:

- Sell winners too fast (lock in gains to avoid the pain of watching them reverse)

- Hold losers too long (refuse to “make it real” by selling)

- Freeze during crashes (paralyzed by potential regret)

- Chase safety over strategy (avoiding pain becomes the primary goal)

- Check their portfolios obsessively during downturns (pain-seeking behavior)

Your brain hates losing so much it would rather fail slowly than succeed steadily. This is literally why most people suck at money: they’re optimizing for avoiding pain rather than building wealth.

The math is simple: if you sell every winner that goes up 20% and hold every loser that goes down 50%, you’ll end up broke even if you pick winners 60% of the time. Loss aversion destroys returns.

What to do instead

- Predetermine your sell rules when you’re calm and rational

- Track outcomes, not feelings (emotions lie; spreadsheets don’t)

- Accept volatility as the price of admission to higher returns

- Reframe losses as tuition in the university of investing

- Focus on position sizing so no single loss is catastrophic

Sin #6 — Confirmation Bias: You Only Believe What You Want to Hear

This one destroys investors because it creates echo chambers of delusion. Confirmation bias explains why most people suck at money even when they’re doing research — because they’re not actually researching, they’re just finding reasons to feel right.

This is how confirmation bias works:

- You only watch videos that confirm your opinion

- You ignore signals that contradict your thesis

- You cherry-pick “evidence” that supports your position

- You treat opinions as data

- You remember the predictions you got right and forget the ones you bombed

This is how people end up married to bad stocks, holding through multiple -50% drawdowns while insisting “the fundamentals are still strong!” Narrator: The fundamentals were not strong.

According to research on confirmation bias in investing, investors selectively gather and interpret information in ways that confirm their pre-existing beliefs. It’s not conscious lying — it’s unconscious filtering. And it’s devastating.

This is precisely why most people suck at money: they’ve surrounded themselves with information that makes them feel smart rather than information that makes them accurate.

What to do instead

- Read arguments against your positions (especially from smart people)

- Force yourself to answer: “What am I missing?” before every purchase

- Stop chasing content that only makes you feel right

- Seek out bearish analyses even when you’re bullish

- Create a “devil’s advocate” document for each major position

Sin #7 — Impulse: The ‘Screw It, I’m Buying It’ Button

Impulse is why:

- You buy stocks after 2 beers

- You panic-sell during a lunch break

- You invest based on vibes, not strategy

- You chase shiny objects

- You make your biggest financial mistakes between 10 PM and 2 AM

Behavioral finance shows that impulsive investors underperform — badly. In fact, research on trading frequency demonstrates that the most active traders (driven by impulse) underperform passive investors by approximately 6.5% annually.

Why? Because impulse is your brain demanding immediate gratification in an arena that rewards delayed gratification. It’s trying to satisfy an emotional itch by making financial decisions. That’s like trying to fix your marriage by buying a sports car.

Impulsivity is amplified by modern technology. Robinhood-style apps are literally designed to trigger impulsive behavior with gamification, instant execution, and dopamine-triggering interfaces. This is why most people suck at money in 2025: the tools have gotten easier, but the psychological traps have gotten more sophisticated.

What to do instead

- Add a 24-hour waiting rule before big moves

- Keep your investment accounts out of sight (delete the app if you must)

- Review your long-term plan weekly, not daily

- Separate “play money” from serious investing capital

- Never trade when emotional, tired, drunk, or hungry

The Good News: You Don’t Have to Be Good at Money to Get Rich

Here’s the secret that explains why most people suck at money — and why you don’t have to be one of them:

You just have to stop sabotaging yourself.

If you can avoid these 7 sins — just avoid them — you’re already ahead of 90% of investors.

Understanding why most people suck at money isn’t about feeling superior. It’s about recognizing that you’re fighting against millions of years of evolution that optimized your brain for survival, not wealth accumulation. Your ancestors who hoarded resources, feared losses, and followed the crowd lived to reproduce. Your ancestors who took calculated risks with abstract future payoffs? They got eaten by something with teeth.

But here’s what changes everything: awareness breaks the pattern.

You don’t need a PhD. You don’t need insider info. You don’t need a supercomputer.

You just need:

- Consistency (showing up matters more than being brilliant)

- Discipline (doing the boring thing when emotions scream otherwise)

- A plan (written down, reviewed regularly, followed religiously)

- The ability to ignore your inner caveman when the charts go red

Do those four things and one day you’ll look around and realize…

You don’t suck at money anymore.

And the beautiful irony? Once you stop sucking at money because of psychology, the actual investing part becomes almost boring. Which is exactly how it should be.

The reason why most people suck at money is that they’re constantly fighting themselves. Stop fighting. Build systems that remove emotions from the equation. Automate what you can. Predetermine your responses to market conditions. And remember: the market doesn’t care about your feelings, so don’t let your feelings make your market decisions.

Most people suck at money not because the concepts are hard — basic diversification and long-term investing aren’t exactly quantum physics. They suck at it because they’re human, and being human comes with buggy psychological software that crashes when markets get volatile.

But now you know why most people suck at money. You’ve seen the seven psychological sins laid bare. The question is: are you going to keep committing them, or are you going to join the small minority who actually builds lasting wealth?

The choice, as always, is yours.

Frequently Asked Questions

Q: Why do most people suck at money even when they’re smart?

Intelligence and financial success aren’t the same thing. Why most people suck at money has nothing to do with IQ and everything to do with emotional control, discipline, and avoiding psychological traps. Smart people often suck at money because they’re overconfident, assuming their general intelligence will transfer to investing without studying behavioral finance principles.

Q: What’s the #1 reason why most people suck at money?

Fear and loss aversion are the biggest culprits. Most people suck at money because they sell during crashes (when they should be buying) and sit on the sidelines during recoveries (when they should be invested). The emotional pain of losing money drives irrational decisions that compound over time.

Q: Can you stop sucking at money if you’ve made mistakes in the past?

Absolutely. Understanding why most people suck at money is the first step toward fixing it. Past mistakes are just expensive education. The key is implementing systems that prevent emotion-driven decisions: automation, predetermined rules, written plans, and accountability mechanisms.

Q: Do professional investors suck at money too?

Many do! Studies show that most active fund managers underperform passive index funds over 10+ year periods. Why most people suck at money applies even to professionals — they’re human too, subject to the same cognitive biases, career pressures, and emotional responses as everyone else.

Q: How long does it take to stop sucking at money?

Behavioral change takes 60-90 days of consistent practice, but true financial discipline develops over years. The good news: once you implement systems that account for why most people suck at money, results compound. Most investors see measurable improvement within 12-24 months of applying behavioral finance principles.

Q: Is it possible to completely eliminate emotional investing?

No, and that’s not the goal. The goal is managing emotions, not eliminating them. Understanding why most people suck at money helps you build guardrails: waiting periods, position limits, written plans, and automated systems that reduce emotional decision-making without requiring you to become a robot.

Q: What’s the difference between fear and rational risk assessment?

Fear is emotional and immediate; rational assessment is analytical and measured. Why most people suck at money is they can’t distinguish between the two. Rational risk assessment involves probabilities, position sizing, and planning. Fear involves panic, checking portfolios obsessively, and making decisions to relieve anxiety rather than build wealth.