Private credit was the cool, exclusive club of the finance world. You know the type: velvet ropes, secret handshakes, and minimum investments that cost more than your house. It was where the “sophisticated” investors played, far away from the prying eyes of regulators and the grubby hands of retail traders.

Well, the lights just came on. And we saw the bugs.

Jamie Dimon, CEO of JPMorgan Chase and professional worrier-in-chief, issued a warning back in October that should have made everyone sit up straight. After two major private credit borrowers collapsed within weeks of each other, he dropped what might be the most memorable financial metaphor since “irrational exuberance”:

“When you see one cockroach, there are probably more.”

Six months later, those cockroaches are scurrying everywhere. The $2 trillion private credit market is having its worst identity crisis since the 2008 financial crisis, and this time, regular investors might be holding the bag. Let’s break down three brutal lessons from this mess, and why your “boring” portfolio might be the smartest move you ever made.

Lesson 1: When You See One Cockroach in Private Credit, There Are Always More

Let’s start with the origin story of Dimon’s bug problem.

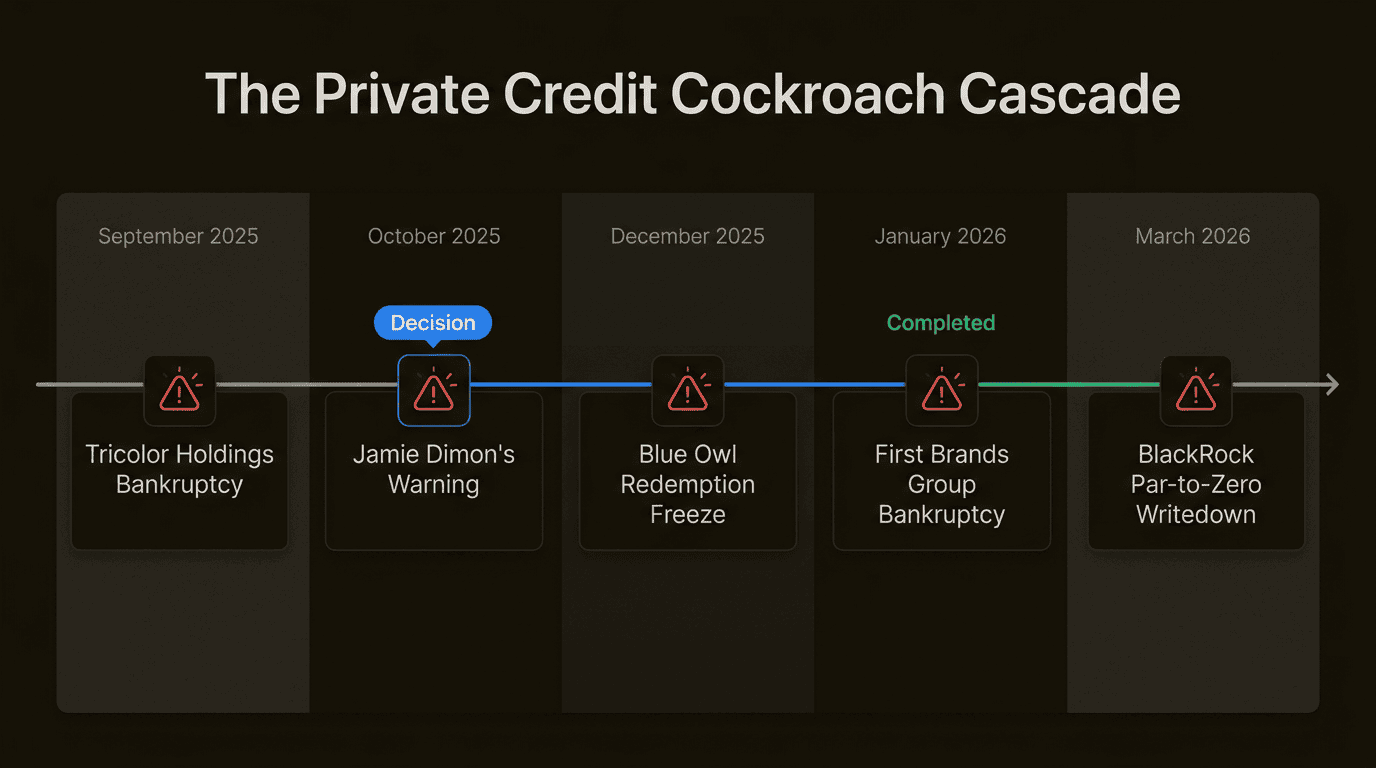

In September 2025, two companies collapsed within weeks of each other, sending shockwaves through the private credit ecosystem. First was Tricolor Holdings, a subprime auto lender that specialized in making loans to risky borrowers with little or no documentation. Tricolor filed for Chapter 7 bankruptcy on September 10 after its lending operations unraveled amid fraud concerns.

Just 18 days later, First Brands Group (an auto parts manufacturer backed by Apollo Global Management) filed for Chapter 11. The company made spark plugs, windshield wipers, filters, and brake components. Banks including UBS O’Connor and Jefferies Financial Group had extended hundreds of millions to both companies before they imploded.

Dimon’s antenna went up immediately. “My antenna goes up when things like that happen,” he told analysts. “And I probably shouldn’t say this, but when you see one cockroach, there are probably more.”

Here’s why the cockroach theory applies so perfectly to private credit. These loans aren’t random one-offs. They’re made during the same market conditions, underwritten with similar assumptions, and often funded by the same pool of capital. When lending standards get loose (and they always do when money is cheap), they get loose across the board. You don’t get one bad loan. You get a portfolio of them.

The Tricolor and First Brands collapses weren’t isolated incidents. They were canaries in the coal mine. And since then, the bugs have kept crawling out.

The Blue Owl Meltdown: A Case Study in Denial

If you want to see what happens when private credit goes sideways, look at Blue Owl Capital. The company has become the poster child for this crisis, and not in a good way.

Blue Owl’s stock is down 34% year-to-date as of March 2026. Over the past year, it’s fallen 48%. But stock prices are just the appetizer. The main course came in February when Blue Owl permanently halted redemptions for its $1.6 billion Blue Owl Capital Corp. II fund. Investors who wanted their money back were told, essentially, “tough luck.”

The fund, structured as a Business Development Company (BDC), announced it would stop offering quarterly redemptions and instead return capital periodically as it winds down the portfolio. CEO Craig Packer called this a “strategic transaction.” Investors called it something else entirely.

Activist hedge funds Saba Capital Management and Cox Capital Partners launched tender offers to buy shares from desperate investors at a discount. When activists are circling like vultures, you know things are bad.

Blue Owl co-CEO Marc Lipschultz tried to push back on the doom and gloom. Speaking at the CAIS Alternative Investment Summit, he quipped: “There might be a lot more cockroaches at JPMorgan.” He called broad concern about private credit “an odd kind of fear-mongering.”

Here’s the thing about denial: it works great until it doesn’t. When liquidity vanishes in private credit, it doesn’t trickle away. It evaporates overnight. And when that happens, “strategic transactions” start looking a lot like panic.

Lesson 2: Private Credit’s Opacity Is a Feature, Not a Bug (And That’s the Problem)

Let’s talk about what private credit actually is, because most people have no idea. And that’s by design.

Private credit refers to direct lending arrangements between non-bank institutional investors and middle-market companies. Instead of going to a bank or issuing public bonds, companies borrow directly from private equity firms, asset managers, and specialized lenders.

This brings us to the BlackRock writedown that should terrify anyone paying attention. In March 2026, BlackRock disclosed that it had written down a $25 million loan to Infinite Commerce (an Amazon storefront aggregator) from 100 cents on the dollar to zero. Here’s the kicker: just 90 days earlier, that same loan had been marked at par.

Ninety days. Par to zero.

That’s the opacity problem in action. In private credit, loans can appear perfectly fine right up until the moment they’re worthless. There’s no gradual decline, no warning signs visible to outside investors.

The Opacity Problem

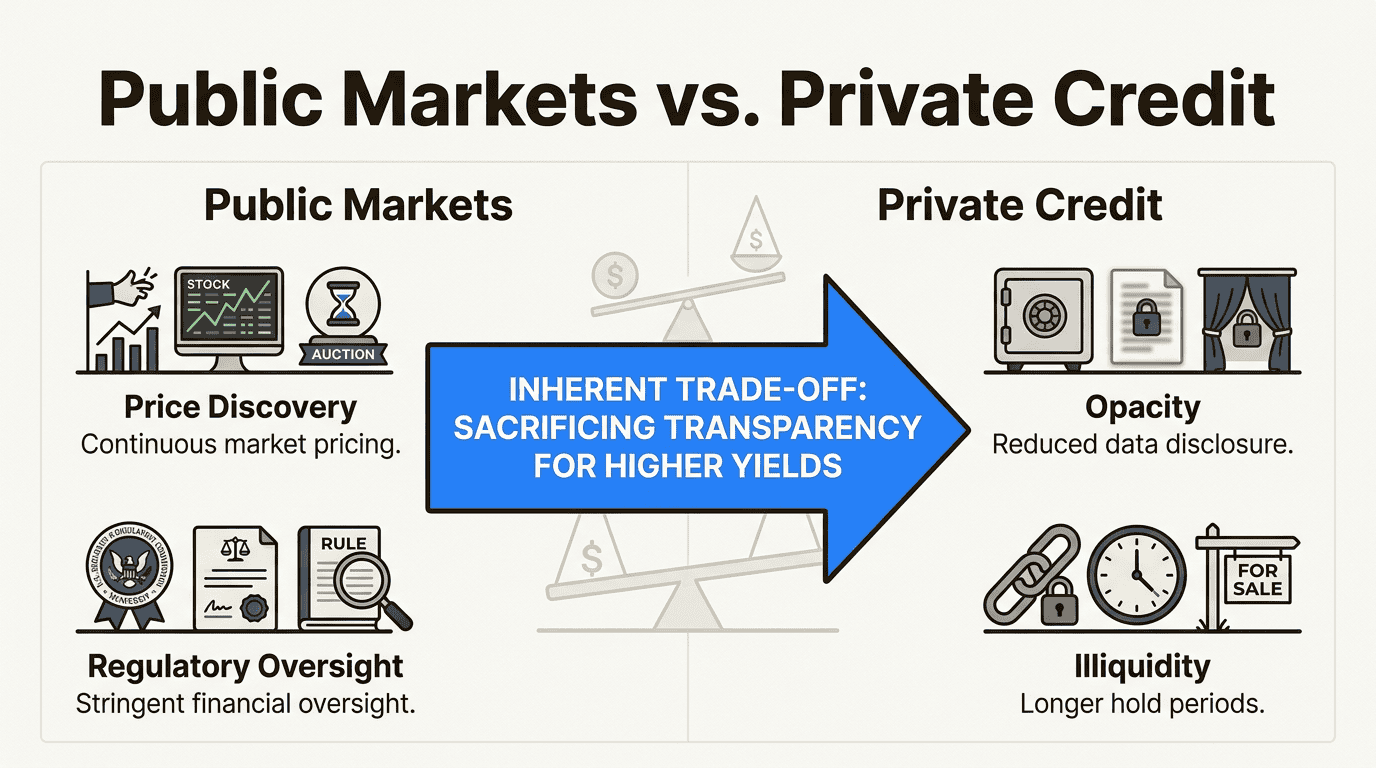

In public markets, prices are discovered continuously. Bonds trade, stocks trade, and you can see exactly what something is worth at any moment. In private credit, there is no price discovery. Loans sit on balance sheets marked at whatever value the lender thinks is reasonable.

As John Mousseau, chief investment officer for Cumberland Advisors, put it: “The prices are a best guesstimate on what things are worth.”

This brings us to the BlackRock writedown that should terrify anyone paying attention.

In March 2026, BlackRock disclosed that it had written down a $25 million loan to Infinite Commerce (an Amazon storefront aggregator) from 100 cents on the dollar to zero. Here’s the kicker: just 90 days earlier, that same loan had been marked at par. Perfectly healthy. Nothing to see here.

Ninety days. Par to zero.

That’s the opacity problem in action. In private credit, loans can appear perfectly fine right up until the moment they’re worthless. There’s no gradual decline, no warning signs visible to outside investors. Just a footnote in an SEC filing that says, “Oh, by the way, that thing we said was worth $25 million? It’s actually worth nothing.”

Moody’s estimates that banks hold roughly $300 billion in loans to private credit issuers, with hundreds of billions more in commitments. Federal Reserve data shows loans to non-depository financial institutions stand at $1.7 trillion. The tentacles of private credit reach everywhere, even into supposedly “safe” banking institutions.

The “SaaS Apocalypse” Complication

As if fraud and opacity weren’t enough, private credit has another problem: AI disruption.

Enterprise software companies have been a favorite target for private credit lenders since 2020. The business model was attractive. Steady recurring revenue, high margins, and a need for growth capital without diluting equity. But then AI happened.

UBS analysts estimate that 25-35% of the private credit market is exposed to AI disruption. iCapital estimates software companies account for roughly 20% of outstanding private-direct loans. The concern is simple: AI tools (like Claude Code and other coding assistants) could erode software company revenues by enabling customers to build in-house solutions instead of buying enterprise software.

The market is already pricing in this risk. The iShares Expanded Tech-Software Sector ETF is down 18% in 2026. When your borrowers’ entire business model is being disrupted by technology, those “safe” loans start looking a lot riskier.

Lesson 3: In Private Credit, Retail Investors Are the Bagholders

Here’s the dirty secret Wall Street doesn’t want you to know: private credit isn’t just for institutions anymore.

In August 2025, President Trump signed an Executive Order allowing individual investors more access to “alternative” offerings, including private markets, in their 401(k) accounts. The stated goal was “democratizing access to alternative assets.” The unstated reality? Wall Street needed new bagholders for its illiquid, opaque, high-fee products.

Tyler Gellasch, president and CEO of Healthy Markets, captured the retail investor dilemma perfectly: “It’s going to be extremely hard for a dentist in Toledo, Ohio, to have a similar understanding of the risk.”

The “Dentist in Toledo” Problem

Tyler Gellasch, president and CEO of Healthy Markets (a nonprofit investor trade group), captured the retail investor dilemma perfectly:

“Some of the most sophisticated, thoughtful, well-trained, well-resourced institutions in the world are right now asking themselves: ‘How risky is this bucket of loans, private credit, that we own?’ It’s going to be extremely hard for a dentist in Toledo, Ohio, to have a similar understanding of the risk.”

Think about that. The smartest people on Wall Street are scrambling to figure out what they own. And somehow, retail investors are supposed to understand these complex, opaque instruments sold to them as “sophisticated” alternatives?

John Mousseau of Cumberland Advisors was even blunter: “Whenever they package this stuff for retail clients, it almost always marks the top of a market.”

History rhymes. In 2008, it was mortgage-backed securities sold to investors who didn’t understand them. Today, it’s private credit wrapped in BDC packaging and marketed as “alternative assets” for your retirement account.

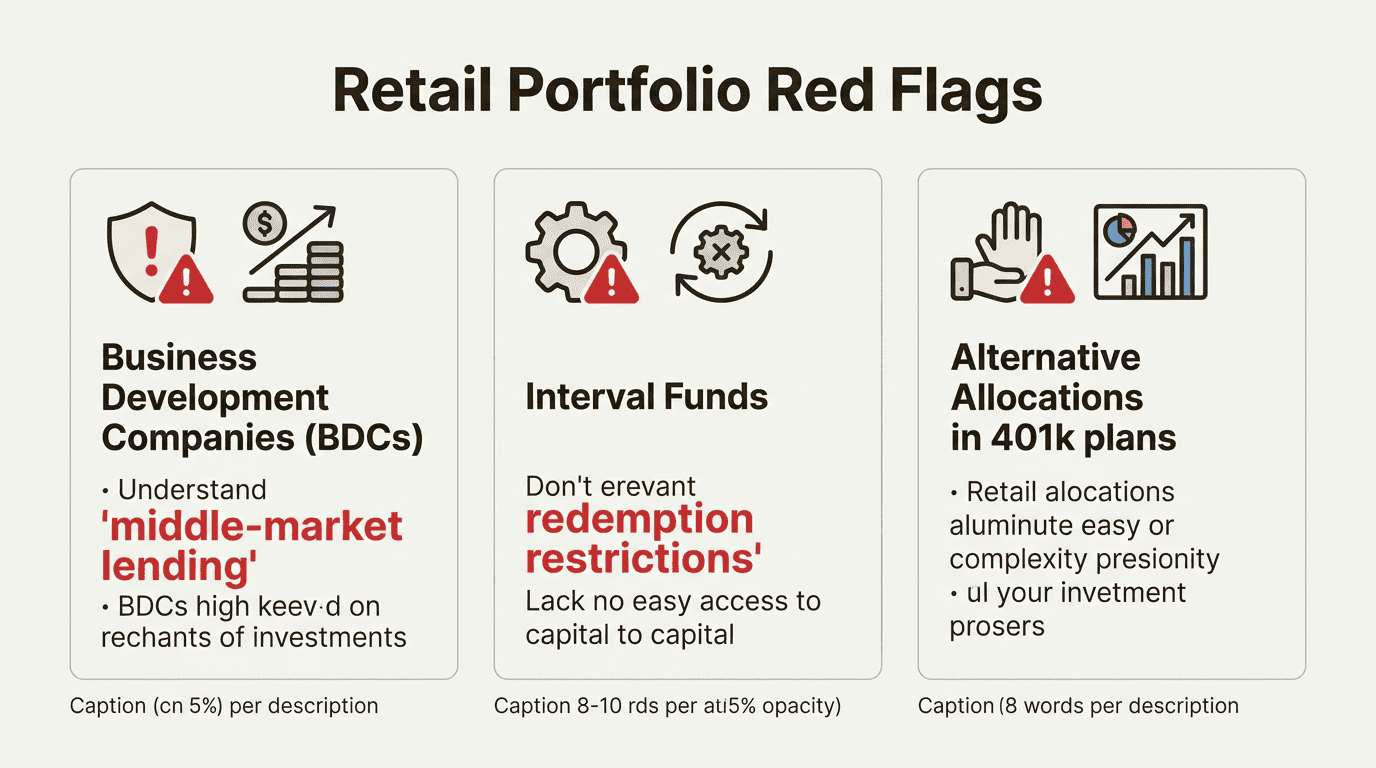

How to Check If You’re Exposed

So how do you know if you’re holding private credit? Here’s where to look:

- Target-date funds: Some now include alternative allocations

- Interval funds: These alternative investment vehicles often hold illiquid private credit

- BDCs in your brokerage account: Look for tickers with “Capital Corp” or similar in the name

- 401(k) alternative options: Check if your plan recently added “alternative” or “private markets” options

Red flags include funds that promise yields significantly higher than comparable bonds, restrictions on redemptions, or holdings described as “middle-market lending” or “direct lending.”

What This Means for Defensive Investors

If you’ve been following The Witty Investor for any length of time, you know our philosophy: boring is beautiful, simple is safe, and complexity is the enemy of the retail investor.

This private credit crisis validates everything we’ve been saying.

The appeal of private credit was always yield. Investors chased those extra percentage points of return and traded away transparency, liquidity, and simplicity to get them. Now they’re learning why those trade-offs exist.

Here’s the thing about transparency: it isn’t just a nice-to-have. It’s how you know what you own. Public markets have price discovery, disclosure requirements, and regulatory oversight because those things protect investors. When you move into opaque private markets, you’re trading away those protections for the promise of higher returns.

Sometimes that trade works. Sometimes you end up holding a loan that goes from par to zero in 90 days.

The Witty Investor Take

Lloyd Blankfein, former CEO of Goldman Sachs, said something in March 2026 that should be etched above every investor’s desk: “The more people say this is overblown, the more you know there’s a problem.”

Blankfein also noted that the current situation “sort of smells like” the eve of the great financial crisis. “I don’t feel the storm, but the horses are starting to whinny in the corral.”

For defensive investors, the playbook doesn’t change:

- Stick to what you can understand

- Prioritize transparency and liquidity

- Remember that yield is compensation for risk (if you don’t know what the risk is, you shouldn’t take it)

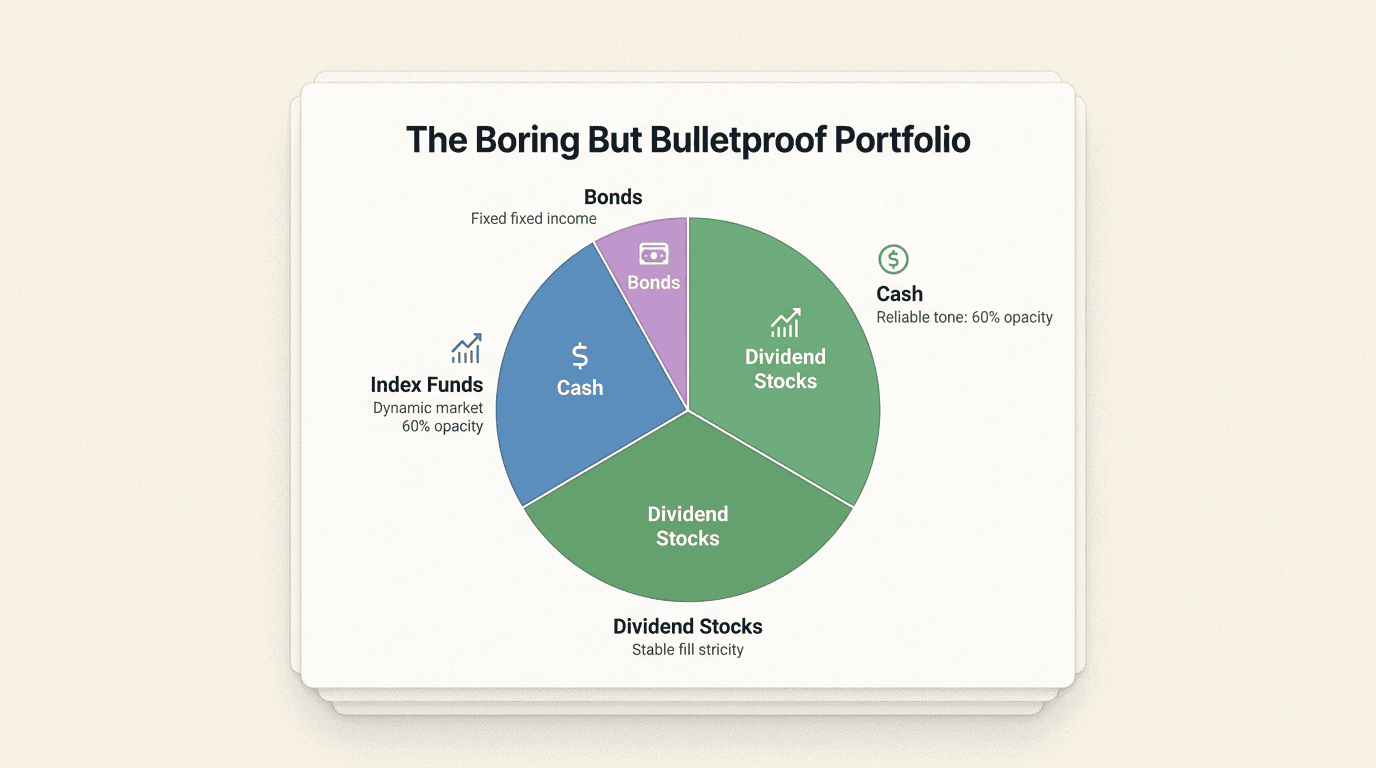

- Keep it simple: dividend stocks, index funds, cash, and maybe some bonds

The “Stay Put Protocol” applies here. Don’t panic. Don’t sell everything because of headlines. But also don’t be naive about what you own. If you discover private credit exposure in your portfolio, understand what you’re holding and whether that risk matches your goals.

Staying Rich Slowly in a World of Financial Cockroaches

Let’s recap the three lessons from this private credit panic:

- Cockroach theory is real: One bad loan means more are hiding. Dimon knew it in October. We’re seeing it play out now.

- Opacity kills: When you can’t see what something is worth, you can’t manage risk. Par-to-zero writedowns in 90 days prove that.

- Retail gets the bill: Wall Street packages complexity for Main Street when institutions get full. Don’t be the bagholder.

Private credit isn’t inherently evil. It’s a legitimate tool for institutional investors with the resources to analyze opaque, illiquid assets. The problem is that it got packaged, marketed, and sold to people who don’t understand what they’re buying.

Wall Street will always find new ways to package risk. Today’s private credit BDCs are yesterday’s mortgage-backed securities. The names change. The pattern doesn’t.

The good news? You don’t need to play this game. You can build wealth with simple, transparent, liquid investments that you actually understand. Dividend stocks that pay you to wait. Index funds that own the whole market. Cash that lets you sleep at night.

Stay rich slowly. Let the cockroaches scurry where they may.

Q1: What is private credit and why is it in crisis?

A1: Private credit refers to direct lending between non-bank investors and middle-market companies, outside traditional banking and public markets. The crisis emerged when major borrowers like Tricolor Holdings and First Brands Group collapsed in late 2025, revealing widespread lending problems. JPMorgan CEO Jamie Dimon’s “cockroach” warning suggested these failures were just the beginning, and subsequent events have proven him right with redemption freezes, fraud charges, and major writedowns across the $2 trillion market.

Q2: How can retail investors be exposed to private credit?

A2: Retail investors can hold private credit through Business Development Companies (BDCs), interval funds, target-date funds with alternative allocations, and recently expanded 401(k) options that include “alternative assets.” These investments often promise higher yields than traditional bonds but carry significant risks including illiquidity, opacity, and potential redemption restrictions that can lock up your capital when you need it most.

Q3: What did Jamie Dimon mean by the “cockroach” comment about private credit?

A3: Dimon’s “when you see one cockroach, there are probably more” comment means that credit problems rarely appear in isolation. When lending standards get loose, they get loose across the board. The Tricolor and First Brands bankruptcies weren’t isolated incidents but early signals of broader problems in private credit underwriting. Since his October 2025 warning, we’ve seen additional failures, fraud revelations, and liquidity crises that validated his concern.

Q4: Why is opacity such a problem in private credit markets?

A4: Unlike public markets where prices are discovered continuously through trading, private credit loans sit on balance sheets with valuations based on “best guesstimates.” BlackRock’s writedown of a $25 million loan from par to zero in just 90 days demonstrates how private credit valuations can mask true risk until it’s too late. Without price discovery, investors can’t assess what their holdings are actually worth or sell them if they want out.

Q5: Should defensive investors avoid private credit entirely?

A5: For most retail investors, yes. Private credit is appropriate for sophisticated institutional investors with resources to analyze complex, illiquid, opaque assets. When packaged for retail through BDCs and 401(k) alternatives, the complexity outweighs the benefits. Defensive investors should prioritize transparency, liquidity, and simplicity: dividend stocks, index funds, cash, and high-quality bonds that you can understand and sell when needed.

Q6: What warning signs should investors watch for in their portfolios?

A6: Look for funds promising yields significantly higher than comparable bonds, redemption restrictions or gates, holdings described as “middle-market lending” or “direct lending,” and recent additions of “alternative” or “private markets” options in your 401(k). If you can’t explain what a fund owns in simple terms, you probably shouldn’t own it.

Frequently Asked Questions

What is private credit and why is it in crisis?

Private credit refers to direct lending between non-bank investors and middle-market companies, outside traditional banking and public markets. The crisis emerged when major borrowers like Tricolor Holdings and First Brands Group collapsed in late 2025, revealing widespread lending problems. JPMorgan CEO Jamie Dimon’s ‘cockroach’ warning suggested these failures were just the beginning, and subsequent events have proven him right with redemption freezes, fraud charges, and major writedowns across the $2 trillion market.

How can retail investors be exposed to private credit?

Retail investors can hold private credit through Business Development Companies (BDCs), interval funds, target-date funds with alternative allocations, and recently expanded 401(k) options that include ‘alternative assets.’ These investments often promise higher yields than traditional bonds but carry significant risks including illiquidity, opacity, and potential redemption restrictions that can lock up your capital when you need it most.

What did Jamie Dimon mean by the ‘cockroach’ comment about private credit?

Dimon’s ‘when you see one cockroach, there are probably more’ comment means that credit problems rarely appear in isolation. When lending standards get loose, they get loose across the board. The Tricolor and First Brands bankruptcies weren’t isolated incidents but early signals of broader problems in private credit underwriting. Since his October 2025 warning, we’ve seen additional failures, fraud revelations, and liquidity crises that validated his concern.

Why is opacity such a problem in private credit markets?

Unlike public markets where prices are discovered continuously through trading, private credit loans sit on balance sheets with valuations based on ‘best guesstimates.’ BlackRock’s writedown of a $25 million loan from par to zero in just 90 days demonstrates how private credit valuations can mask true risk until it’s too late. Without price discovery, investors can’t assess what their holdings are actually worth or sell them if they want out.

Should defensive investors avoid private credit entirely?

For most retail investors, yes. Private credit is appropriate for sophisticated institutional investors with resources to analyze complex, illiquid, opaque assets. When packaged for retail through BDCs and 401(k) alternatives, the complexity outweighs the benefits. Defensive investors should prioritize transparency, liquidity, and simplicity: dividend stocks, index funds, cash, and high-quality bonds that you can understand and sell when needed.

What warning signs should investors watch for in their portfolios?

Look for funds promising yields significantly higher than comparable bonds, redemption restrictions or gates, holdings described as ‘middle-market lending’ or ‘direct lending,’ and recent additions of ‘alternative’ or ‘private markets’ options in your 401(k). If you can’t explain what a fund owns in simple terms, you probably shouldn’t own it.