At-a-Glance: Medtronic (MDT) 2026 Fundamentals

| Metric | Q3 2026 Status | The Witty Take |

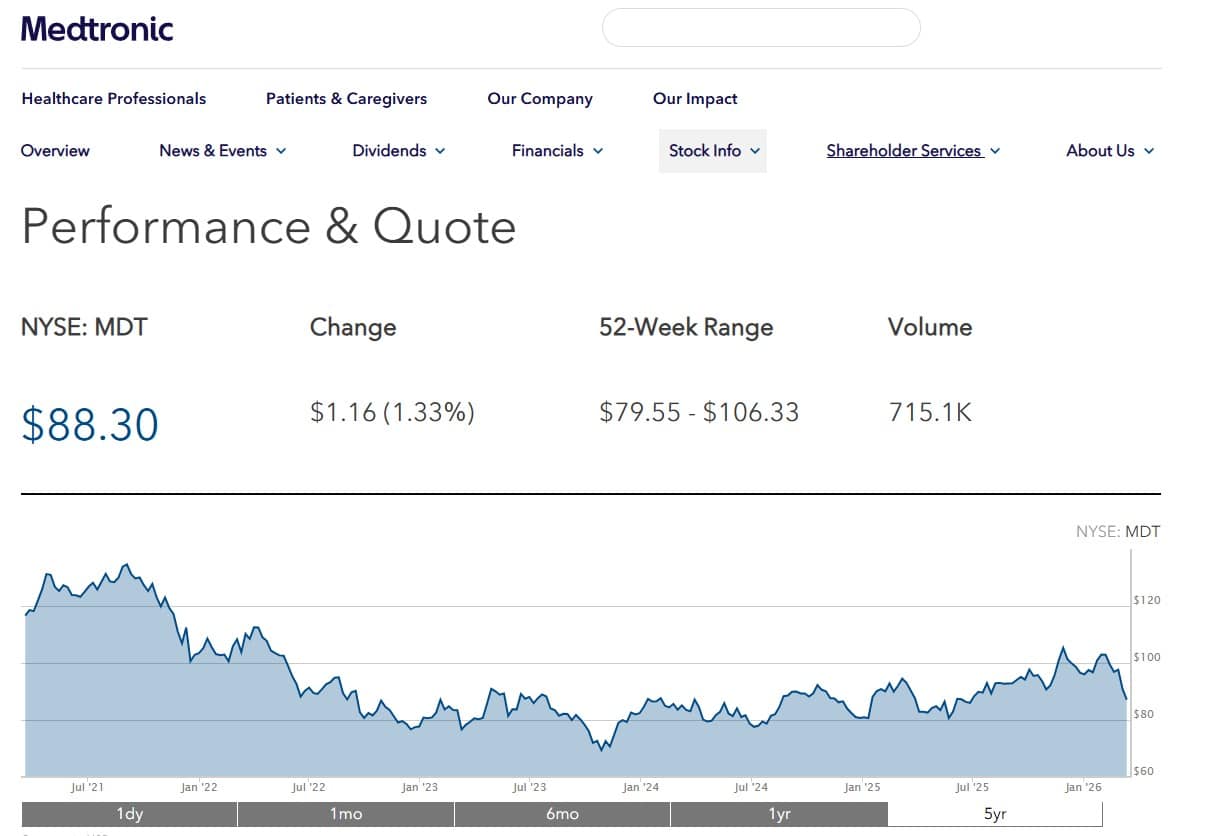

| Current Price | ~$87.38 | Trading at a 6-8% intrinsic discount |

| Price Target | $110.00 | ~22.8% potential upside |

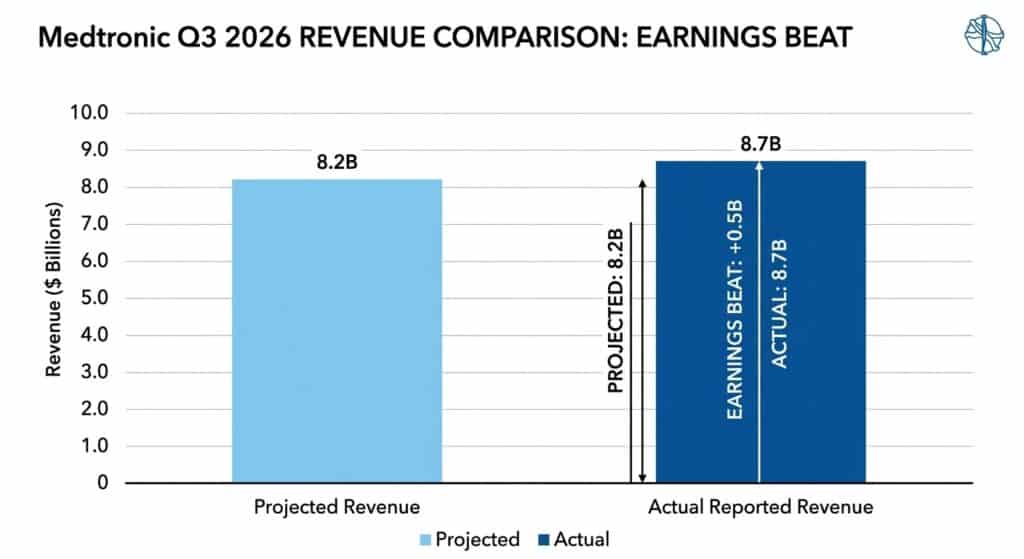

| Q3 2026 Revenue | $9.02 Billion | Beat consensus estimates; 6% organic growth |

| Dividend Yield | ~3.26% ($0.71/qtr) | Reliable passive income generator |

| Key Catalyst 1 | Pulsed Field Ablation | PFA sales grew >300% YoY in Q2/Q3 |

| Key Catalyst 2 | Hugo Surgical Robot | Secured US FDA clearance; first surgeries underway |

Medtronic Stock Analysis: Is MDT Witty or Risky in 2026?

A comprehensive Medtronic stock analysis reveals that the company is a highly compelling buy, currently trading at a discount near $87 with a clear path to a $110 consensus price target. Propelled by massive 300% growth in its Pulsed Field Ablation division and recent FDA clearance for its Hugo surgical robot, Medtronic combines defensive market stability with aggressive technological innovation. For investors seeking reliable income, its 48-year streak of dividend increases makes it an elite, foundational anchor for any long-term portfolio.

While the broader market in 2026 has been bouncing around like a caffeinated squirrel on a trampoline, Medtronic (NYSE: MDT) has quietly continued doing what it has done for decades: building critical life-saving medical devices, generating massive, reliable cash flow, and paying shareholders steadily increasing dividends.

But numbers alone don’t tell the whole story. A proper Medtronic stock analysis requires understanding what the company actually does, how it makes money in the trenches of the healthcare system, and why its products matter in the real world.

Let’s dig in.

The Witty Investor’s Golden Rule

Building wealth isn’t about chasing the flashiest, most volatile meme stock. My strict rule is to rely on the boring, battle-tested companies—the ones that stubbornly refuse to fail, no matter what the economy is doing.

That exact same philosophy applies to building wealth.

Most Wall Street reports on a Medtronic stock analysis read like they were written by a committee of sleep-deprived analysts locked inside a fluorescent conference room—endless jargon and charts that explain nothing. Instead, look at Medtronic through the lens of survival infrastructure.

Medtronic isn’t a speculative biotech startup promising miracle cures in five years. It’s a global medical device powerhouse. Pacemakers. Surgical robotics. Neurological implants. These are not optional technologies that hospitals can cut from the budget when the economy dips; they are absolute necessities. Conducting a fundamental Medtronic stock analysis reveals that infrastructure companies like this tend to produce the most reliable, sleep-well-at-night investments.

Understanding Medtronic’s Growth Engine

Before deciding whether the stock is Witty or Risky, an accurate Medtronic stock analysis must break down the core divisions currently driving the company’s 2026 revenue beats.

1. Cardiovascular Devices & The PFA Boom

Heart disease remains the leading cause of death worldwide. Medtronic’s cardiovascular division produces pacemakers, defibrillators, and heart valves. But the real story here—and the reason any modern Medtronic stock analysis should turn bullish—is Pulsed Field Ablation (PFA).

PFA is used to treat atrial fibrillation (AFib), an irregular heartbeat condition. Traditional methods used heat or extreme cold (cryoablation) to scar heart tissue. PFA, however, uses non-thermal electrical pulses to selectively target myocardial cells without damaging surrounding tissue like the esophagus or nerves.

The 2026 data is staggering. Medtronic’s PFA sales, driven by their PulseSelect and Sphere-9/Affera systems, grew by more than 300% year-over-year in recent quarters. PFA now accounts for an incredible 75% of the company’s cardiac ablation revenue. In a $12 billion electrophysiology market, Medtronic is rapidly stealing market share from competitors, entirely justifying a positive outlook in our Medtronic stock analysis.

2. Neuroscience Innovations

Medtronic produces a variety of neurological implants and surgical tools used to treat conditions such as Parkinson’s disease, chronic pain, and epilepsy. Because these therapies require long-term treatment, hospitals continue buying related hardware and replacement components. This creates the sticky, recurring revenue streams that dividend investors love to see in a Medtronic stock analysis.

Medtronic Hugo Robotic Surgery: The Next Frontier

A major catalyst that demands attention in this Medtronic stock analysis is the Hugo robotic-assisted surgery (RAS) platform. Robotic surgery is one of the fastest-growing areas in medicine, allowing surgeons to perform delicate procedures with higher precision and smaller incisions.

For years, Intuitive Surgical (makers of the da Vinci robot) held a near-monopoly. That is officially changing.

In late 2025, the FDA cleared the Hugo RAS system for urologic surgical procedures (like prostatectomies and nephrectomies). By February 2026, the first U.S. commercial surgical cases were successfully performed at the prestigious Cleveland Clinic.

What makes Hugo special? It features a modular, cart-based design, meaning hospitals can move the robotic arms between different operating rooms rather than dedicating a massive suite to a single machine. It also integrates seamlessly with Medtronic’s AI-powered “Touch Surgery” ecosystem. As Medtronic seeks further FDA approvals for gynecological and general surgeries, this Medtronic stock analysis projects the Hugo system will be a massive revenue driver for the second half of the decade.

Q3 2026 Financials: Running the Numbers

A Medtronic stock analysis is only as good as the hard data supporting it. Let’s look at the most recent Q3 Fiscal 2026 earnings report from February.

- Revenue: $9.02 Billion (a 5.8% year-over-year increase, beating the $8.89B consensus).

- Organic Growth: 6.0% (driven heavily by the cardiovascular and medical-surgical divisions).

- Earnings Per Share (EPS): $1.36 adjusted, beating the expected $1.34.

- Strategic Moves: Medtronic recently announced its intent to acquire CathWorks, bolstering its interventional cardiology pipeline.

These results show something incredibly important for our Medtronic stock analysis: Medtronic consistently executes. In a market that punishes missed earnings, Medtronic delivered solid top-line growth and reaffirmed its full-year guidance of $5.62–$5.66 EPS. While they face some margin pressures from supply chain costs and tariffs, their operating cash flow remains a massive $4.8 billion, providing plenty of capital for R&D and shareholder returns.

Medtronic Stock Dividend History: The Income Investor’s Dream

If you are building wealth for the long haul, the crown jewel of any Medtronic stock analysis is the company’s immaculate dividend profile.

Let’s talk about consistency. As of 2026, Medtronic has increased its dividend for 48 consecutive years.

That means the company has raised its payout through the high inflation of the late 70s, the dot-com crash, the 2008 financial crisis, the COVID-19 pandemic, and recent interest rate hikes. Few companies on earth maintain that level of financial discipline.

Currently, Medtronic pays a $0.71 quarterly dividend, yielding around 3.26%. This payout is heavily supported by their strong free cash flow generation. They are just two years away from achieving elite “Dividend King” status (50 years of consecutive increases). When conducting a Medtronic stock analysis for a retirement or passive income portfolio, this level of reliability is practically unmatched in the healthcare sector.

Valuation & Potential Risks

One reason value investors are flocking to this Medtronic stock analysis in 2026 is the pricing gap. At roughly $87 per share, the stock trades at a value score that suggests an intrinsic discount. Most major analyst narratives peg the fair value between $95 and $110, creating a potential upside of up to 22.8%.

However, no Medtronic stock analysis is complete without acknowledging the risks on the horizon:

- Regulatory Pressure: Medical devices must pass rigorous FDA approvals. If a device like the Hugo robot faces a recall or if the PulseSelect system has safety issues, the financial impact is immediate and severe.

- Fierce Competition: Boston Scientific has aggressively entered the PFA market, doubling its market share recently. Medtronic must continue to out-innovate heavyweights like Johnson & Johnson and Abbott Laboratories.

- Margin Contraction: Rising costs of raw materials and global tariffs have slightly squeezed Medtronic’s gross margins in 2026, though high-margin tech like PFA helps offset this.

The Witty Verdict: Is Medtronic a Good Long Term Investment?

When you step back and view the big picture of this Medtronic stock analysis, several undeniable themes emerge. Global healthcare spending is rising. Populations are aging rapidly. The demand for advanced medical technology—from robotic surgery to cardiac ablation—is permanently baked into our future.

Medtronic will probably never be the hottest, trendiest stock on Wall Street. It won’t appear in meme stock forums or promise to revolutionize artificial intelligence overnight. Instead, it quietly manufactures the foundational medical infrastructure that keeps millions of people alive, and then it sends its shareholders a larger dividend check every single year.

Final Rating: Witty for dividend investors. A highly strategic, defensive play with a solid margin of safety for value investors.

FAQ: Medtronic Stock Analysis

Is Medtronic stock a Dividend King?

Not quite yet, but they are incredibly close. A thorough Medtronic stock analysis shows the company has 48 consecutive years of dividend increases. Dividend King status requires 50 years. Barring a catastrophic financial event, they are fully on track to join that elite group by 2028.

How does Medtronic Hugo robotic surgery compare to Intuitive’s da Vinci?

While Intuitive Surgical’s da Vinci has dominated the market for over two decades, Medtronic’s Hugo offers a unique modular, cart-based design that allows hospitals more flexibility. Recent FDA clearances in late 2025 for urologic procedures make Hugo a legitimate, highly competitive alternative in the robotic surgery space.

Is Medtronic a good long term investment for 2026 and beyond?

Yes. Healthcare companies with sticky revenue streams, aggressive innovation pipelines (like PFA and surgical robotics), and near half-century dividend growth streaks are the definition of strong defensive investments. Our Medtronic stock analysis concludes that buying at the current mid-$80s valuation offers a great entry point for long-term compounding.

What is Pulsed Field Ablation (PFA) and why does it matter for Medtronic?

PFA is a groundbreaking treatment for atrial fibrillation that uses electrical pulses instead of thermal energy to treat heart tissue, vastly improving safety and procedure times. It is the fastest-growing segment in Medtronic’s portfolio, with PFA sales up over 300% recently, completely disrupting a $12 billion global market.

Keep Reading Before You Do Something Expensive

If you’re digging into Medtronic stock analysis, there’s a good chance you’re also trying to build a portfolio that doesn’t collapse the moment the market gets indigestion. These next reads will help:

- Best Dividend Stocks for March 2026: Expert Picks

Looking for more reliable income plays beyond Medtronic? This roundup covers dividend stocks with strong payouts, durable businesses, and fewer nasty surprises. - Behavioral Finance vs Behavioral Economics: 7 Brutal Truths for Investors

Learn why your brain keeps trying to sabotage your portfolio, and why understanding investor behavior matters just as much as reading balance sheets. - Why Smart People Still Lose Money in the Stock Market

A helpful reminder that intelligence alone won’t save you from panic-selling, overconfidence, or buying garbage at the top.