AbbVie (ABBV): Is This Dividend Tank Built to Survive After Humira?

AbbVie’s been called a one-drug wonder for years — and that drug, Humira, is finally fading into retirement. But before you start writing AbbVie’s obituary, take a look at the company’s replacement lineup. Between Skyrizi and Rinvoq, this “dividend tank” might just have enough horsepower to keep rolling over the competition — and keep your portfolio paid in the process.

Quick Take

AbbVie is basically saying, “Yeah, Humira is aging out, and we don’t even care.” The company’s new anti-inflammatory drugs Skyrizi and Rinvoq are exploding in sales, and management says those two alone could bring in around $25 billion in 2025 and more than $31 billion by 2027. For investors watching AbbVie stock, this transition is the story that defines whether ABBV remains a buy or becomes a cautionary tale. Yahoo Finance | Seeking Alpha

Meanwhile, shareholders are still getting paid: AbbVie’s quarterly dividend is $1.64 per share (that’s $6.56 per year), which works out to roughly a 2.8–2.9% yield right now, and the company has raised that dividend every year for 11 straight years. The most recent ex-dividend date was October 15, 2025, with the next cash payout scheduled for November 14, 2025. StockAnalysis | AbbVie Investor Relations

So… income investors love AbbVie stock, growth investors are circling it, and panic investors are like “wait I thought Humira was dead, how is this thing still up?”

Let’s break it down.

Understanding AbbVie Stock: The Post-Humira Era

Revenue Transition Timeline (2022-2027E)

1. What Does AbbVie Actually Sell Now?

For years AbbVie stock = Humira. Humira was the best-selling drug on planet Earth and pulled in over $21 billion in 2022. But then biosimilar competition hit in the U.S. in 2023, and Humira sales are now in freefall (down more than 50% year over year in recent quarters). Reuters: Biosimilar Competition

Here’s the plot twist: AbbVie knew this was coming and built replacements.

Skyrizi (for psoriasis, Crohn’s, etc.)

Rinvoq (for rheumatoid arthritis and a growing list of autoimmune diseases)

Q2 2025 Revenue Snapshot: The Handoff is Complete

| Drug | Q2 2025 Revenue | Year-over-Year Change | Status |

|---|---|---|---|

| Skyrizi | $4.4 billion | ↑ 45%+ | 🚀 Primary Growth Driver |

| Rinvoq | $2.0 billion | ↑ 55%+ | 🚀 Explosive Growth |

| Humira | $1.2 billion | ↓ 50%+ | 📉 Declining Legacy |

| Total Immunology | $7.6 billion | ↑ Net Positive | ✅ Transition Working |

Source: AbbVie Q2 2025 Earnings Report

That’s the handoff in real time. Investors tracking AbbVie stock are watching this portfolio shift closely because it determines whether ABBV can maintain growth post-Humira.

AbbVie also just flexed in a head-to-head study: Rinvoq beat Humira in rheumatoid arthritis outcomes, which is wild because AbbVie is basically replacing its own legend with something better — and locking in market exclusivity on Rinvoq out to 2037 after a settlement with would-be generics. That extended protection could add billions in future sales. Reuters: Patent Settlement

Translation: The “Humira cliff” didn’t kill AbbVie stock. It just forced AbbVie to evolve.

2. Is AbbVie Stock Still Growing, or Just Milking Cash?

Growing.

AbbVie brought in about $15.4 billion in revenue in Q2 2025, up ~6.6% year over year, and raised full-year guidance because demand for Skyrizi and Rinvoq keeps beating expectations. Adjusted earnings per share for that quarter came in at $2.97, up ~12% from last year, and above Wall Street estimates. For anyone analyzing AbbVie stock, these numbers matter because they prove the transition strategy is working. MarketWatch

Management also bumped their 2025 profit outlook higher and says they still expect high single-digit revenue growth through 2029. That’s not “we’re dying,” that’s “we’re still compounding.” AbbVie Investor Relations

AbbVie Stock Performance Metrics (Q2 2025)

| Metric | Q2 2025 | Q2 2024 | Change | Wall Street Expectation |

|---|---|---|---|---|

| Revenue | $15.4B | $14.5B | +6.6% | Beat |

| Adjusted EPS | $2.97 | $2.65 | +12.1% | Beat |

| Operating Margin | ~38% | ~36% | +2pp | In-line |

| Skyrizi Revenue | $4.4B | $3.0B | +46.7% | Beat |

| Rinvoq Revenue | $2.0B | $1.3B | +53.8% | Beat |

Sources: AbbVie Earnings | NASDAQ

For Q3 2025 (the quarter they’re about to report), AbbVie guided to around $15.5 billion in net revenue and adjusted EPS of $1.74–$1.78. Investors will be watching two questions:

- Are Skyrizi and Rinvoq still accelerating?

- How fast is Humira shrinking?

If those first two drugs keep outrunning the Humira decline, Wall Street stays calm, and dividend investors keep nodding like “continue.”

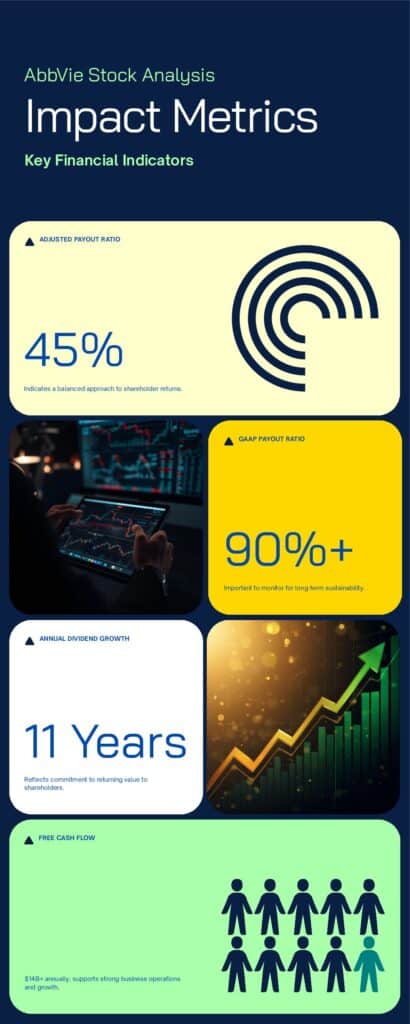

3. Let’s Talk Dividend, Because I Know That’s Why You’re Here

AbbVie stock is an income machine, and that’s a major reason why dividend investors keep ABBV on their radar.

Current quarterly dividend: $1.64/share

Annualized: $6.56/share

Yield right now: ~2.8–2.9% (this floats with the stock price)

Streak: 11 straight years of dividend increases since AbbVie was spun out of Abbott Labs.

StockAnalysis Dividend History | AbbVie Dividend News

AbbVie Stock Dividend History (2014-2025)

| Year | Annual Dividend | Increase % | Yield at Year-End | Stock Price Range |

|---|---|---|---|---|

| 2014 | $1.60 | Baseline | ~3.2% | $55-65 |

| 2016 | $2.28 | +42.5% | ~3.5% | $58-68 |

| 2018 | $4.28 | +87.7% | ~4.8% | $85-105 |

| 2020 | $5.20 | +21.5% | ~5.2% | $95-115 |

| 2022 | $5.92 | +13.8% | ~3.9% | $145-175 |

| 2024 | $6.20 | +4.7% | ~3.1% | $175-210 |

| 2025 | $6.56 | +5.8% | ~2.9% | $215-240 |

Sources: StockAnalysis | Seeking Alpha

Not only are they still paying, they keep raising. AbbVie historically bumps the dividend in Q4, and analysts are already whispering about another ~5–6% hike in late 2025 to keep the “we are a shareholder-return company” narrative intact. Seeking Alpha: Dividend Analysis

Why This Matters for AbbVie Stock Investors:

Plenty of “high yield” pharma names pay you 5%+ but the stock goes nowhere or bleeds.

AbbVie stock is trying to pay you AND still grow earnings.

That combo is rarer than finance TikTok wants you to believe.

Is the payout ratio high on paper? Yes — GAAP payout looks huge because pharma accounting includes chunky R&D milestones and acquisition costs that smash GAAP earnings. But on an adjusted cash/operating basis, AbbVie says the dividend is covered and growing alongside Skyrizi/Rinvoq sales. BioSpace: AbbVie Financial Analysis

In normal-people English: They’re not paying the dividend out of desperation, they’re paying it out of confidence.

Dividend Sustainability Score for AbbVie Stock

4. What Could Break This Story?

Let’s be adults for a second about AbbVie stock.

Risk #1: Dependence on 2 Drugs

AbbVie stock is now heavily concentrated in Skyrizi and Rinvoq. If regulators, safety data, or competitors hit either of those, the “we’re fine after Humira” story cracks. The company is racing to widen Rinvoq’s and Skyrizi’s approved uses (more diseases = bigger moat), but that’s still clinical and regulatory risk. Reuters: Drug Development

Risk #2: Pricing / Political Pressure

AbbVie lives in immunology, neurology, and aesthetics. U.S. drug pricing is under constant political attack. (If you think politicians won’t threaten Big Pharma pricing power in an election cycle, welcome to America.) Any forced price cuts on autoimmune drugs would get Wall Street’s attention fast. Kaiser Health News: Drug Pricing

Risk #3: “Peak Rinvoq / Skyrizi” Hype

Wall Street is already baking in monster numbers: management says >$31B combined in 2027 for those two drugs, up from a previous “just” $27B. If growth slows before we get there, AbbVie stock can pull back hard. Seeking Alpha: Revenue Projections

AbbVie Stock Risk Matrix

| Risk Factor | Probability | Impact if Realized | Mitigation Strategy | Investor Watch Items |

|---|---|---|---|---|

| Skyrizi/Rinvoq safety issues | Low-Medium | Severe | Ongoing clinical trials | FDA announcements |

| Regulatory setbacks | Medium | High | Label expansion efforts | Pipeline updates |

| Drug pricing regulation | High | Medium-High | Diversification | Legislative news |

| Competition | Medium | Medium | Patent protection to 2037 | Biosimilar approvals |

| Revenue miss vs. guidance | Low-Medium | Medium | Conservative guidance | Quarterly earnings |

| Dividend cut | Very Low | Severe | Strong cash flow | Cash flow statements |

Sources: FDA | BioPharma Dive

In other words, AbbVie stock is still executing. But expectations are now high. When expectations are high, misses get punished.

5. So… Is AbbVie Stock “Witty or Risky?”

Let’s do it:

Witty (Bull Case for AbbVie Stock)

✅ Skyrizi + Rinvoq are doing exactly what they were built to do: replace Humira and keep cash flowing.

✅ Management is guiding for continued revenue and EPS growth into 2029. AbbVie Investor Relations

✅ Dividend keeps climbing. You’re literally getting paid while the company reinvents itself. StockAnalysis | Seeking Alpha

✅ Rinvoq patent protection now stretches to 2037, which is forever in biotech years. Reuters: Patent News

✅ Proven execution on product transitions – AbbVie has successfully navigated one of the most challenging patent cliffs in pharmaceutical history.

Risky (Bear Case for AbbVie Stock)

⚠️ You are betting heavily on two drugs carrying a multi-hundred-billion-dollar company. If anything dents those drugs, AbbVie stock bleeds. Seeking Alpha: Risk Analysis

⚠️ Political heat on drug pricing can nuke margins faster than a TikTok ban rumor nukes social media stocks. Fierce Pharma: Pricing Pressure

⚠️ The yield (~2.8–2.9%) is good, but it’s not 5%. You’re here for dividend growth, not max raw yield. StockAnalysis: Yield Comparison

⚠️ High expectations – Wall Street is already pricing in aggressive growth through 2027.

My Read for This Wednesday:

AbbVie stock is still in “Witty.”

This isn’t a dying high-yield trap. This is an R&D machine that survived losing one of the biggest drugs in history and is still telling Wall Street, “Yeah, we’ll keep growing and yes, you still get raises.”

Could that change? Absolutely. Will I keep watching it? Also absolutely.

Analyst Consensus on AbbVie Stock (October 2025)

| Rating | Number of Analysts | Percentage | Average Price Target |

|---|---|---|---|

| Strong Buy | 8 | 32% | $250-270 |

| Buy | 12 | 48% | $235-250 |

| Hold | 4 | 16% | $215-235 |

| Sell | 1 | 4% | $190-210 |

| Consensus | 25 Total | 80% Positive | $242 |

Sources: Yahoo Finance Analyst Ratings | MarketBeat

Bottom Line for Investors

If you’re an income-focused long-term investor, AbbVie stock still deserves a spot on your watchlist / watchlist-plus. You’re not buying Humira. You’re buying Skyrizi, Rinvoq, and the idea that AbbVie knows how to milk a cash cow and breed the next one at the same time.

Key Investment Considerations for AbbVie Stock:

✅ BUY if you:

- Want dividend growth with capital appreciation

- Believe in AbbVie’s product transition execution

- Have a 5+ year investment horizon

- Can tolerate pharmaceutical sector volatility

⚠️ WATCH if you:

- Need high current yield (5%+) immediately

- Are uncomfortable with drug concentration risk

- Want shorter-term trades

- Are sensitive to political/regulatory headlines

❌ AVOID if you:

- Need guaranteed income without volatility

- Can’t stomach pharmaceutical sector risks

- Believe drug pricing regulation will cripple margins

- Want diversified revenue streams NOW

Where to Learn More About AbbVie Stock

- Official Investor Relations: investors.abbvie.com

- SEC Filings: SEC EDGAR – AbbVie

- Real-Time Quotes: Yahoo Finance ABBV

- Analyst Research: Seeking Alpha ABBV

- Dividend Calendar: Dividend.com AbbVie

- Clinical Trial Pipeline: ClinicalTrials.gov

- Industry News: FiercePharma | BioPharma Dive

Final Verdict on AbbVie Stock

AbbVie stock represents a rare combination in today’s market: a company executing a massive portfolio transition while maintaining and growing its dividend. The successful handoff from Humira to Skyrizi and Rinvoq is no longer theoretical – it’s happening in real-time with revenue numbers to prove it.

For dividend growth investors with patience and a long-term perspective, AbbVie stock offers compelling value. The 2.8-2.9% yield might not turn heads immediately, but combined with consistent dividend raises, solid revenue growth, and extended patent protection through 2037, ABBV builds a strong case for long-term wealth accumulation.

The risks are real – drug concentration, political pressure, and high expectations create legitimate concerns. But if you’re looking for a pharmaceutical dividend stock that’s already proven it can navigate the most challenging patent cliff in industry history, AbbVie stock has earned its place on your research list.

This is not personalized financial advice. I’m not your fiduciary. I’m the loud friend who reads earnings calls so you don’t have to.

“If You Liked This, Read Next”

7 Best Brokerages for Dividend Investing in 2025 (Witty, Wealthy & Worry-Free) – Before you chase yield, make sure your broker isn’t quietly charging you for the privilege. We ranked the smartest platforms for dividend investors who want easy reinvestment, low fees, and zero nonsense.

Market Panic Investing: How Smart Investors Profit When Everyone Else Panics (2025 Edition) – Learn how smart investors turn chaos into opportunity and fear into income streams.

The Psychology of Panic Selling: Why Investors Keep Shooting Themselves in the Foot – Learn how smart investors turn chaos into opportunity and fear into income streams.

Witty or Risky? The Financial Face-Off Series – Learn how smart investors turn chaos into opportunity and fear into income streams.

Disclaimer

This analysis of AbbVie stock is for informational and educational purposes only. It does not constitute investment advice, financial advice, trading advice, or any other type of advice. You should not treat any of the content as such. AbbVie stock investing involves risk, including possible loss of principal. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.