Financial Literacy for Adults: 5 Proven Pillars for 2026

What Is Financial Literacy (and What It Is Not)

Financial literacy is the ability to understand and effectively use financial skills. That includes budgeting, investing, credit management, and long-term planning. It means knowing how to make your money work for you instead of constantly working for your money.

But here is what financial literacy is NOT:

- It is not memorizing a bunch of rules about deprivation

- It is not tracking every penny in a spreadsheet until you die

- It is not becoming a financial monk who never enjoys life

- It is definitely not following advice written by people who inherited their wealth

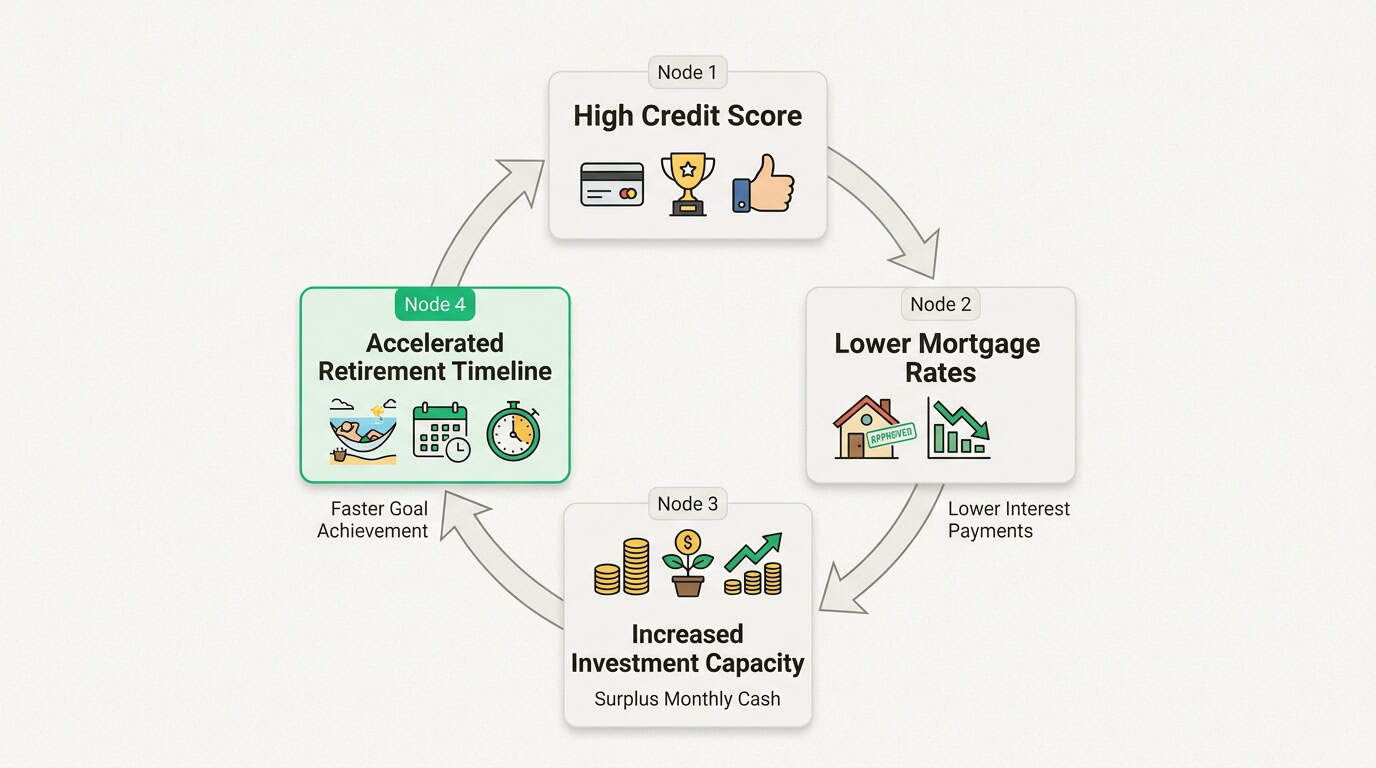

Real financial literacy is about understanding systems. It is knowing why a 401(k) match is literally free money (more on that later). It is understanding that your credit score is not a measure of your worth as a human being, but it does affect your mortgage rate, which affects your monthly payment, which affects how much you can invest, which affects when you can retire.

Everything connects. That is the first lesson of financial literacy.

The FINRA Foundation’s 2024 National Financial Capability Study found that only 46% of Americans have enough savings to cover three months of expenses. That is down from 53% in 2021. Meanwhile, the percentage of adults paying off their credit cards in full every month decreased by 6 percentage points. These are not just statistics. They are warning signs that traditional approaches to financial literacy education are failing.

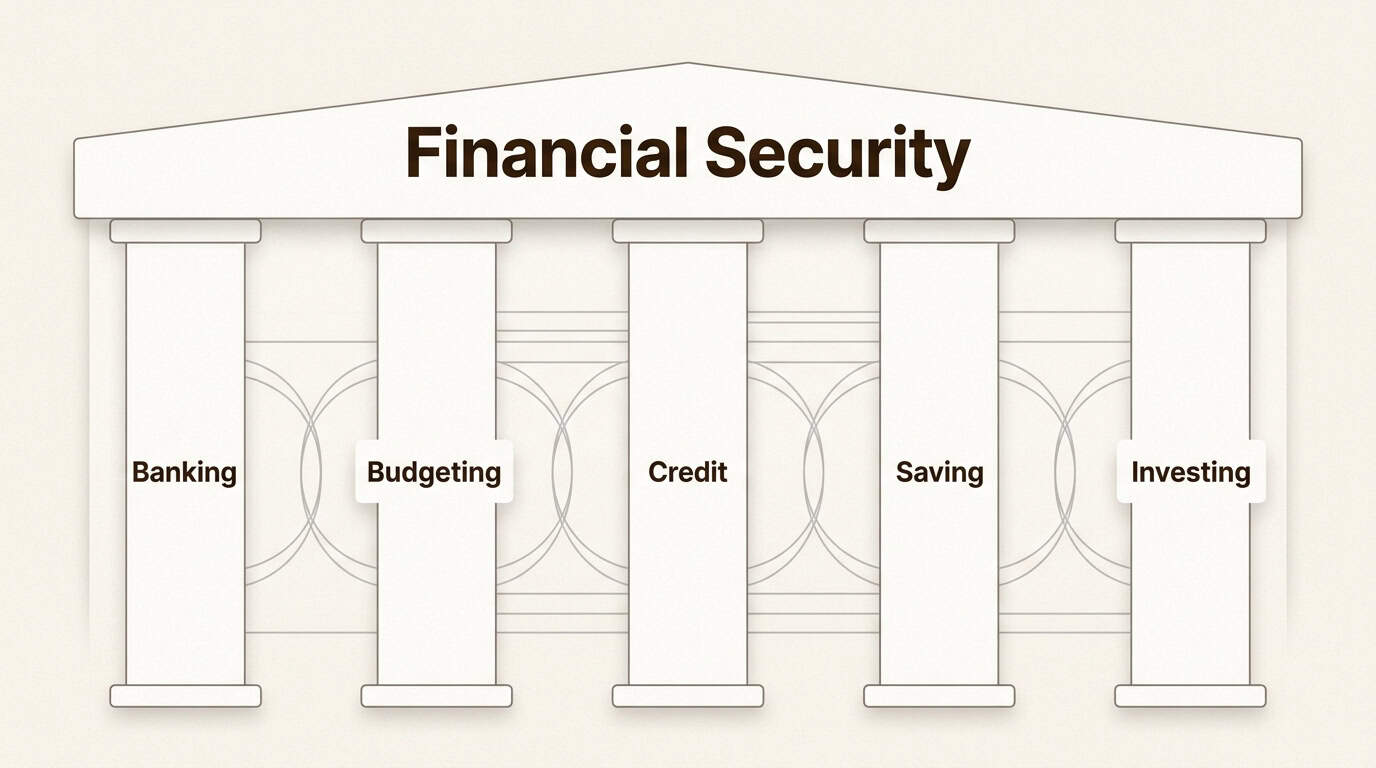

The Five Pillars of Financial Literacy

Every sound financial literacy system rests on five pillars. Miss one, and the whole structure gets wobbly. Let us walk through each one and, more importantly, how they interconnect.

Banking and cash flow systems

Your bank accounts are the foundation. Not exciting, but essential.

Here is the adult version of banking advice: you need a checking account for daily operations, a savings account for short-term goals, and a high-yield savings account for your emergency fund. That is it. Three accounts maximum. Anyone telling you to open seven different accounts for “envelope budgeting” is selling complexity you do not need.

Credit unions versus banks? Credit unions generally offer better rates and lower fees because they are member-owned. Banks offer better technology and more locations. If you rarely visit branches and your credit union has a decent app, go with the credit union. If you travel constantly and need ATM access everywhere, a national bank might make more sense.

The real key to financial literacy is automation. Your paycheck should hit your checking account via direct deposit. From there, automatic transfers should move money to savings and investment accounts before you even see it. Willpower is a finite resource. Systems are not.

Speaking of systems, your emergency fund belongs in a high-yield savings account, not your checking account. The standard advice says three to six months of expenses. Let us be more specific: three months if you have a stable job in a growing industry, six months if you have kids or work in a volatile field. The Federal Reserve Bank of New York reports that total household debt has reached $18.8 trillion. An emergency fund is your insurance policy against becoming another statistic.

Budgeting that actually works

The 50/30/20 rule gets thrown around constantly: 50% for needs, 30% for wants, 20% for savings and debt. Here is how to actually apply it.

First, calculate your actual take-home pay, not your salary. Then categorize your spending honestly. Rent, groceries, utilities, minimum debt payments: those are needs. Restaurants, entertainment, subscriptions: those are wants. The 20% for savings includes retirement contributions, emergency fund building, and extra debt payments.

If your needs are eating up 70% of your income, you have an income problem or a housing problem, not a budgeting problem. No amount of coupon clipping fixes a rent payment that is 50% of your take-home pay.

For variable income earners (freelancers, commission sales, gig workers), budgeting gets trickier. Base your budget on your worst month from the past year, not your average or best month. In good months, bank the excess. In bad months, you have a cushion.

The “pay yourself first” system works like this: automate transfers to savings and investments on payday. What is left in checking is what you have to spend. This flips the script from “save what is left over” to “spend what is left after saving.” Small difference, massive impact over time.

Credit and debt management

Let us talk about debt without the shame spiral that usually accompanies it.

The Federal Reserve’s latest G.19 report shows revolving credit (mostly credit cards) at $1.33 trillion, with average interest rates on assessed accounts at 22.32%. That is not a typo. Twenty-two percent. If you are carrying a balance, every dollar you do not pay off is costing you 22 cents per year.

Here is the hierarchy for debt payoff:

- Minimum payments on everything (protects your credit score)

- Build a $1,000 mini emergency fund (prevents new debt)

- Throw everything at the highest interest debt (avalanche method)

- Snowball into the next highest

The avalanche method (highest interest first) mathematically beats the snowball method (smallest balance first) every time. However, if you have five small debts that would give you psychological wins, the snowball is fine. The difference of a few months in payoff time is less important than actually sticking with the plan.

Credit scores matter, but they are not mysterious. According to Experian, the factors are payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit (10%). Translation: pay on time, keep balances under 30% of limits, do not close old accounts, and do not open a bunch of new accounts at once.

Saving and wealth building

Saving is not investing. They serve different purposes and belong in different accounts.

Savings are for goals within five years: emergency fund, down payment, vacation, next car. This money belongs in high-yield savings accounts or CDs. Current rates vary, but online banks typically offer significantly better rates than brick-and-mortar institutions.

Investing is for goals more than five years away, primarily retirement. This money belongs in the stock market through retirement accounts. Why the five-year distinction? Because the market can drop 20% in a year, and you do not want to need that money when it does.

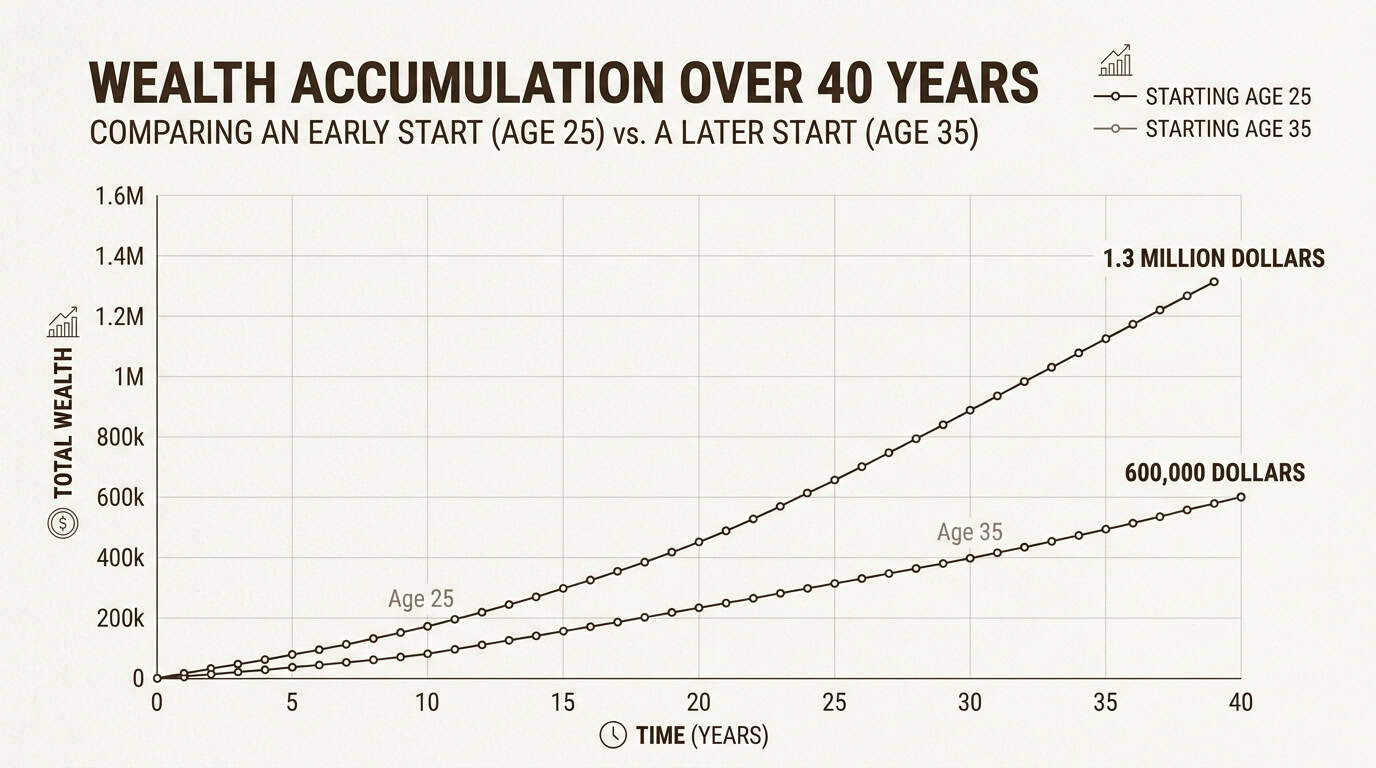

The magic of compound interest is real, but it requires time. Invest $500 monthly from age 25 to 65 at 7% average returns, and you will have about $1.3 million. Start at 35 instead, and you will have about $600,000. That decade cost you $700,000. Time is the ingredient you cannot substitute.

Investing and retirement

If your employer offers a 401(k) match and you are not contributing enough to get the full match, you are leaving free money on the table. Full stop. That is a 100% immediate return on investment.

After capturing the match, the hierarchy looks like this:

- Max out your Roth IRA ($7,500 or $8,600 if 50+ in 2026)

- Increase 401(k) contributions

- Taxable brokerage accounts for additional investing

Why Roth IRA second? Because according to the IRS, Roth contributions grow tax-free forever, and you can withdraw contributions (not earnings) penalty-free if absolutely necessary. It is flexibility with tax advantages.

The 2026 IRA contribution limit is $7,500 ($8,600 if age 50 or older), up from $7,000 in previous years. These limits adjust periodically for inflation, so check current limits before contributing.

For investments, unless you enjoy spending your weekends analyzing balance sheets, stick with low-cost index funds. They automatically diversify your holdings and historically outperform actively managed funds after fees. The difference of 1% in annual fees compounds to hundreds of thousands of dollars over a lifetime.

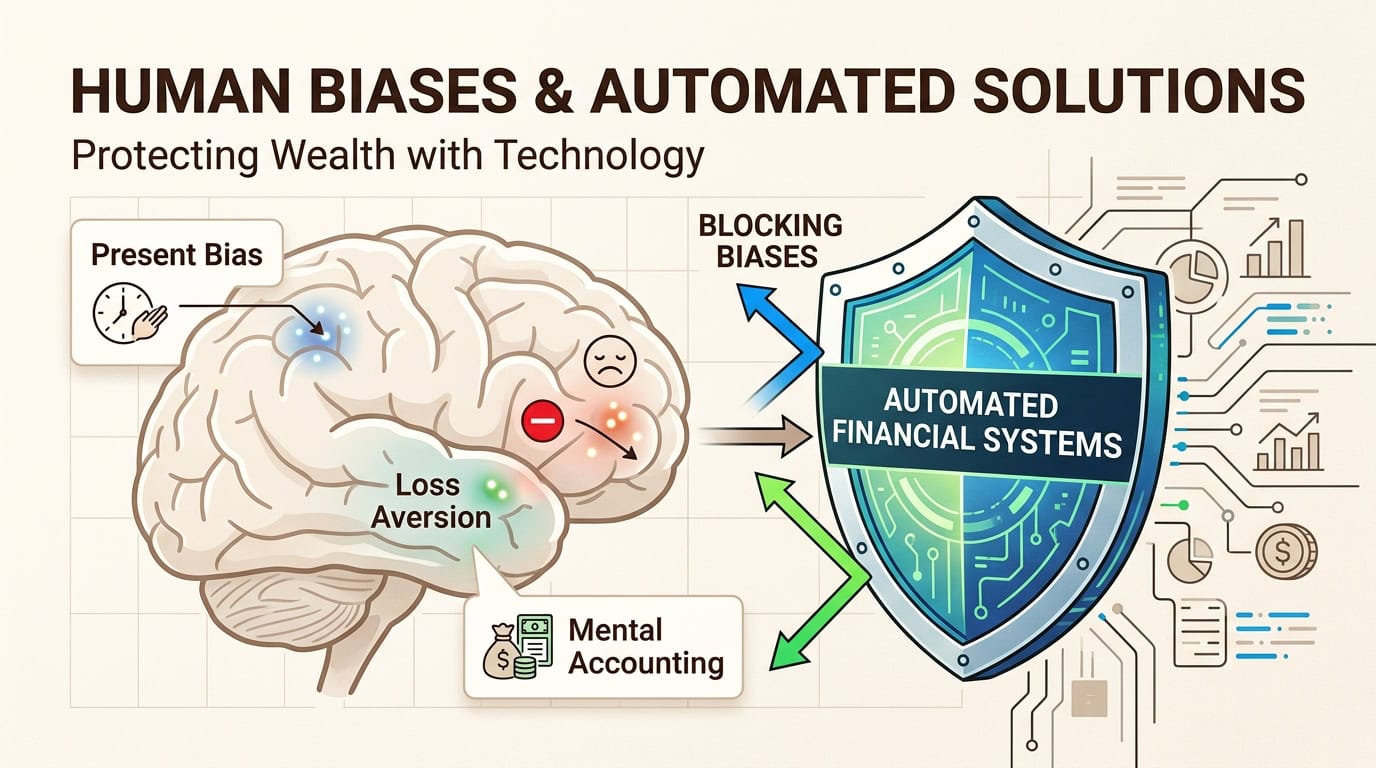

The Psychology of Money: Systems Beat Willpower

Understanding the mechanics of money is only half the battle. The other half is understanding yourself.

Behavioral economics has identified specific cognitive biases that sabotage financial decisions. Present bias makes us value $100 today more than $120 next year, even though that is a 20% return. Loss aversion makes us hold losing investments too long (hoping they recover) and sell winners too early (locking in gains). Mental accounting causes us to treat a tax refund as “found money” to blow, even though it was our money all along.

The solution is not to fight these biases. It is to build systems that work around them.

Automate your savings so you never see the money. Use separate accounts for different goals so your brain treats them as untouchable. Set up automatic investment contributions so you are dollar-cost averaging without thinking about it.

Debt shame is another psychological trap. The financial industry has done an excellent job convincing people that debt is a moral failing. It is not. It is a mathematical situation with mathematical solutions. Yes, you made decisions that got you there. No, dwelling on that does not help you solve it. Focus on the numbers, make a plan, and execute.

Money conversations with partners are uncomfortable but necessary. Schedule a monthly “financial date” to review accounts, discuss goals, and make decisions together. Waiting until there is a crisis ensures you will have the conversation during a crisis, which is never productive.

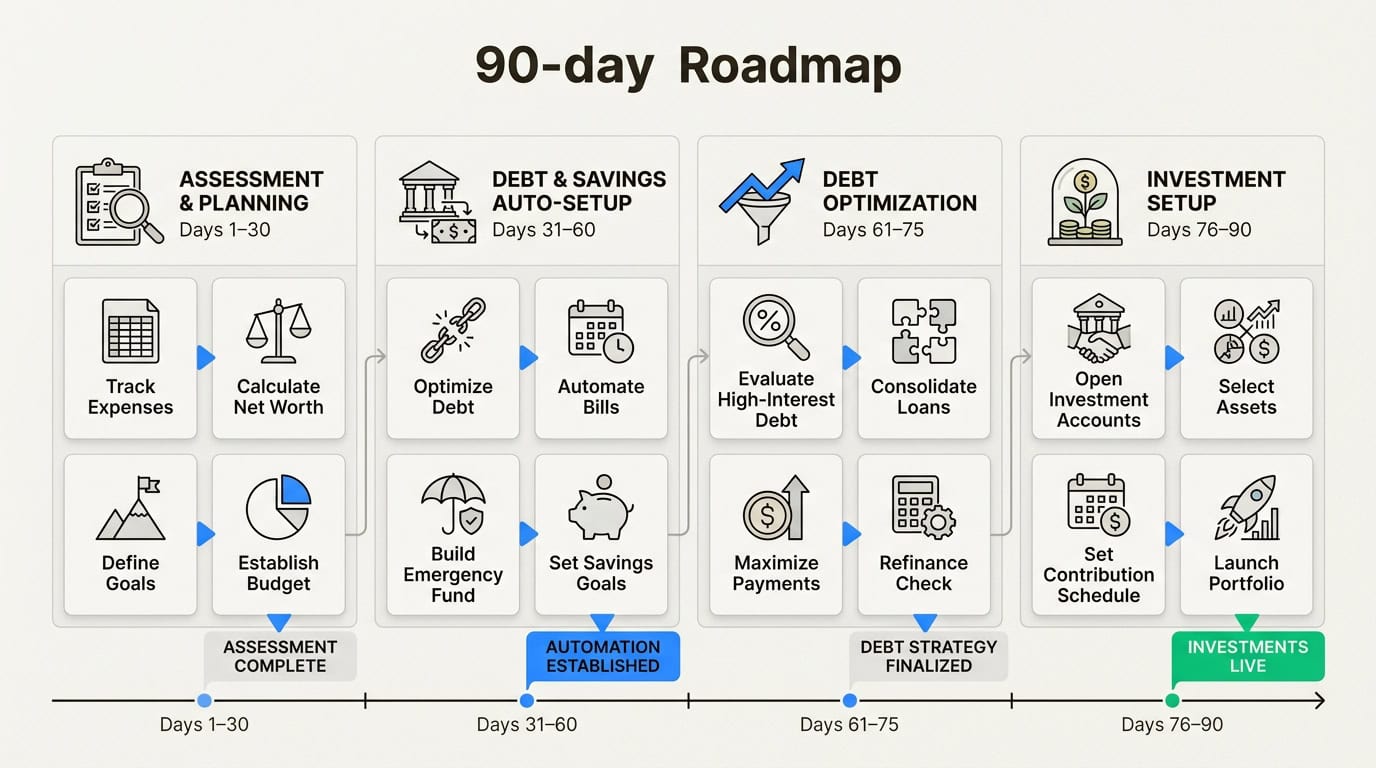

Putting It All Together: Your 90-Day Financial Literacy Action Plan

Knowledge without action is just trivia. Here is how to implement everything we have covered in the next three months.

Weeks 1-2: Assess and Automate

- List every account you have and what it is for

- Set up direct deposit if you have not already

- Open a high-yield savings account for your emergency fund

- Automate a transfer to savings on payday, even if it is just $50

Weeks 3-4: Build the Safety Net

- Get your first $1,000 into that emergency fund

- Check your credit reports at AnnualCreditReport.com (free weekly through 2026)

- List all your debts with balances, minimum payments, and interest rates

Month 2: Optimize Debt and Credit

- Implement your chosen debt payoff strategy

- Set up automatic payments for everything to avoid missed payments

- If your credit utilization is over 30%, focus on paying down balances before other goals

Month 3: Start Investing

- Increase your 401(k) contribution to get the full employer match

- Open a Roth IRA if you do not have one

- Set up automatic monthly contributions to that IRA

Tools that actually help include YNAB for zero-based budgeting, Personal Capital for investment tracking, and your bank’s own automation features. Avoid anything that charges high fees or promises to “optimize” your investments through stock picking.

When should you hire a professional? If you have complex tax situations, own a business, or are within ten years of retirement, a fee-only Certified Financial Planner (CFP) can be worth the cost. Look for someone who charges by the hour or a flat fee, not commissions on products they sell you.

Start Building Your Financial Literacy Foundation Today

Financial literacy is not a destination. It is a continuous practice of making slightly better decisions, month after month, year after year. The goal is not perfection. The goal is progress.

The statistics are sobering. With only 46% of Americans having adequate emergency savings and credit card debt at record highs, the traditional approach to personal finance is clearly not working. But you do not have to be part of that statistic.

Pick one action from this guide and do it this week. Just one. Open that high-yield savings account. Increase your 401(k) contribution by 1%. Check your credit report. Momentum builds momentum.

Twenty years as a systems analyst has taught me that complex problems rarely require complex solutions. They require the right fundamentals applied consistently. The same is true of your money.

Investing is hard. Being bad at it is optional.

Frequently Asked Questions

How long does it take to become financially literate?

You can grasp the fundamentals of financial literacy in a few hours of focused reading. However, applying those concepts and building wealth is a lifelong journey. Expect to spend a few months getting your systems in place, then regular maintenance (monthly check-ins, annual reviews) to stay on track.

What is the most important aspect of financial literacy for beginners?

Understanding the difference between assets and liabilities. Assets put money in your pocket (investments, income-generating property). Liabilities take money out (consumer debt, depreciating vehicles). Building financial literacy starts with focusing your energy on acquiring assets and minimizing liabilities.

Can you improve your financial literacy without spending money on courses?

Absolutely. Resources like the CFPB’s consumer tools, Khan Academy’s free courses, and the FDIC’s Money Smart program provide comprehensive financial literacy education at no cost. Start there before spending money on paid courses.

How does financial literacy impact mental health?

Significantly. The FINRA study found that fewer Americans report satisfaction with their financial condition despite stable financial knowledge. This suggests that financial literacy alone is not enough, but combined with action, it reduces anxiety, improves relationships, and provides a sense of control over your future.

What role does financial literacy play in retirement planning?

A crucial one. The disparity is stark: 80% of college graduates have retirement accounts versus just 37% of those without degrees. Understanding compound growth, tax-advantaged accounts, and employer matching through financial literacy education can mean the difference between a comfortable retirement and working into your 70s.

Is financial literacy more important than earning a high income?

In many ways, yes. Plenty of high earners live paycheck to paycheck because they never developed financial literacy skills. Meanwhile, people with modest incomes who understand budgeting, saving, and investing build substantial wealth over time. Your behavior with money matters more than how much you earn.

How can parents teach financial literacy to their children?

Start with age-appropriate concepts. Young children can learn about saving through piggy banks. Teenagers can manage their own checking accounts and learn about credit before they get their first card. The most powerful tool is modeling good financial behavior yourself, because according to research, 69% of young adults view their parents as their most trusted source for financial advice.

Keep Reading (Before You Go Blow Your Budget on Something Dumb)

- 👉 What Does Palantir Do? (And Should You Actually Invest in It?)

Now that you understand financial basics, here’s how to apply them to a real company without getting lost in buzzwords and hype. - 👉 M1 Finance News 2026: Key Updates, Rate Changes, and What Investors Should Watch

Because your platform matters. Here’s what M1 is changing, what it means for your money, and whether it’s helping you build wealth… or just rearranging the furniture. - 👉 7 Tools I Use to Analyze Stocks Faster (and Smarter)

If you’re ready to move from “I should invest” to “I actually know what I’m doing,” start here.