Your Portfolio Called. It’s Bored.

Most investors build portfolios that look like everyone else’s. Stocks, bonds, maybe some real estate if they’re feeling spicy. Then they wonder why their returns are as exciting as watching paint dry.

Enter timberland investing. Yes, trees. Those things that grow in the ground while you sleep.

Timberland has quietly delivered returns that rival the S&P 500 with roughly half the volatility. It’s an inflation hedge, a portfolio diversifier, and (unlike your crypto holdings) it’s backed by something you can actually touch. Trees don’t disappear in a market crash. They just keep growing.

Here’s the short version: there are five ways to invest in timberland, ranging from “buy a REIT with your lunch money” to “purchase 10,000 acres and become a timber baron.” This guide breaks down each approach, the real risks nobody talks about, and whether timberland deserves a spot in your portfolio in 2026.

What Is Timberland Investing (And Why It Actually Makes Sense)

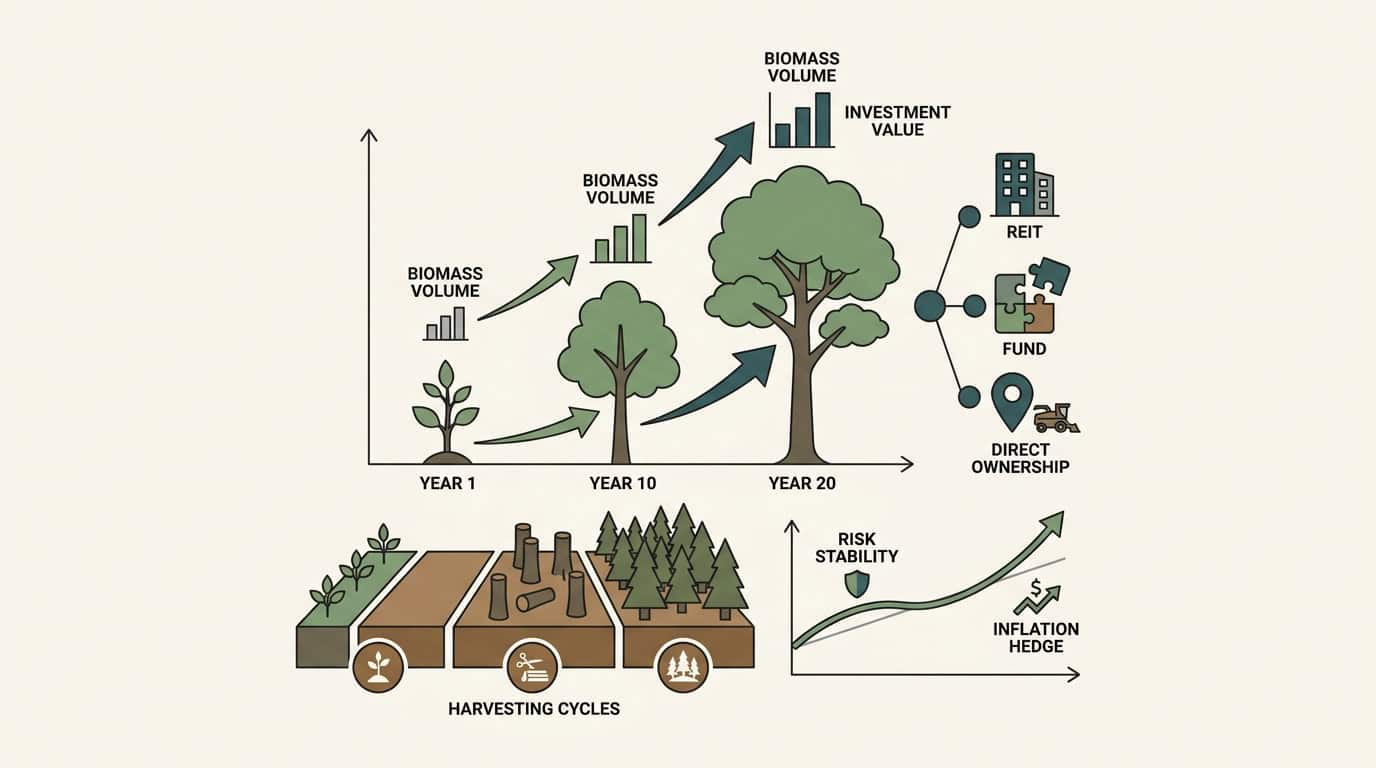

Timberland investing means owning forested land for the purpose of harvesting timber and benefiting from land appreciation. It’s classified as a real asset, similar to raw land or farmland, but with a unique twist: your asset literally grows while you wait.

Here’s why that matters. When you own stocks, you’re hoping the market values them higher tomorrow. When you own timberland, your trees increase in physical volume every year. A 10-year-old pine is worth more than a 5-year-old pine simply because there’s more of it. This biological growth happens regardless of what the Federal Reserve does or whether tech stocks are crashing.

The numbers back this up. According to the NCREIF Timberland Index, timberland returns over the past 20 years have nearly matched the S&P 500. But here’s the kicker: timberland showed less than half the volatility. We’re talking stock-market returns with bond-market stability.

Timberland also serves as an inflation hedge. When prices rise, timber prices typically follow. Land values tend to appreciate during inflationary periods. And because timberland returns move independently of stocks and bonds, adding it to your portfolio reduces overall volatility.

Bottom line? Timberland isn’t exciting. That’s exactly why it works.

5 Ways to Invest in Timberland (From Pocket Change to Private Equity)

Not everyone can (or should) buy 1,000 acres of forest. Fortunately, timberland investing has entry points for every budget and risk tolerance.

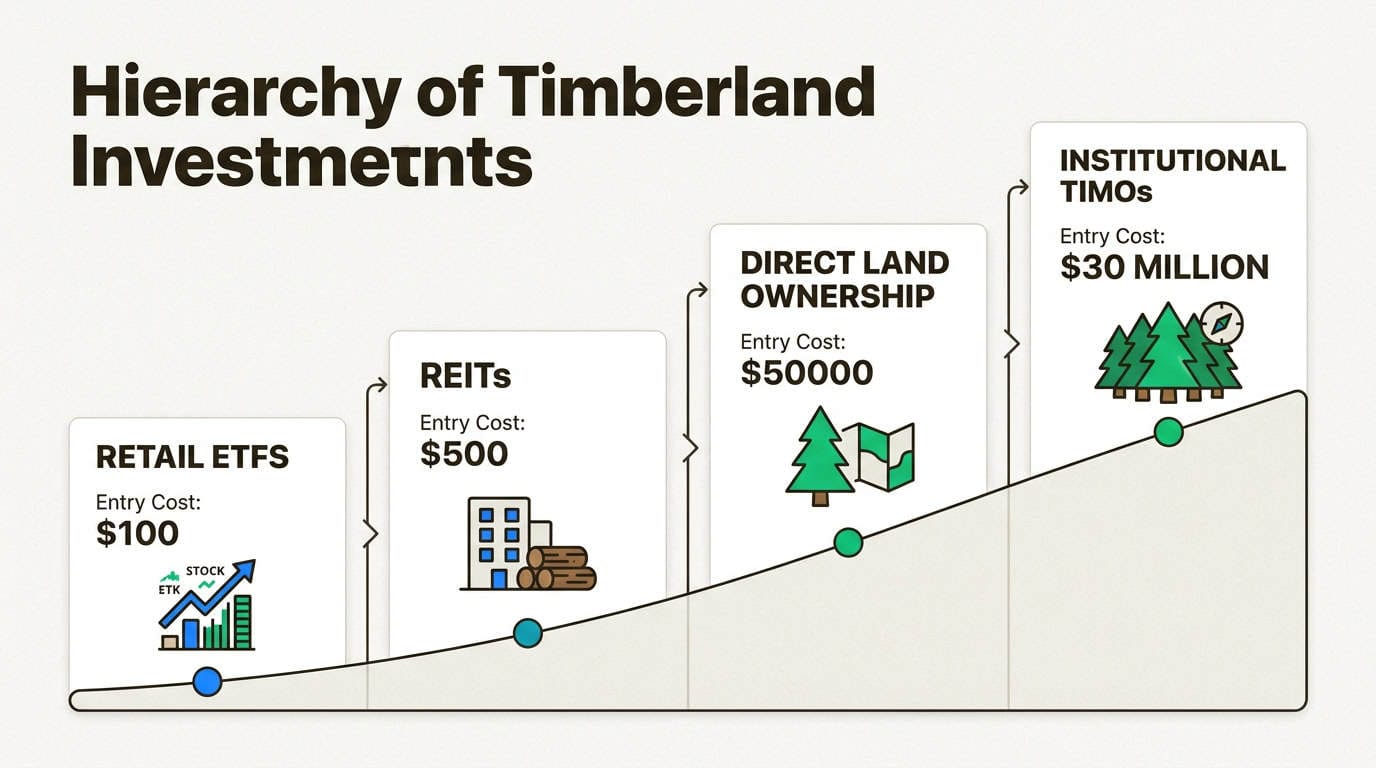

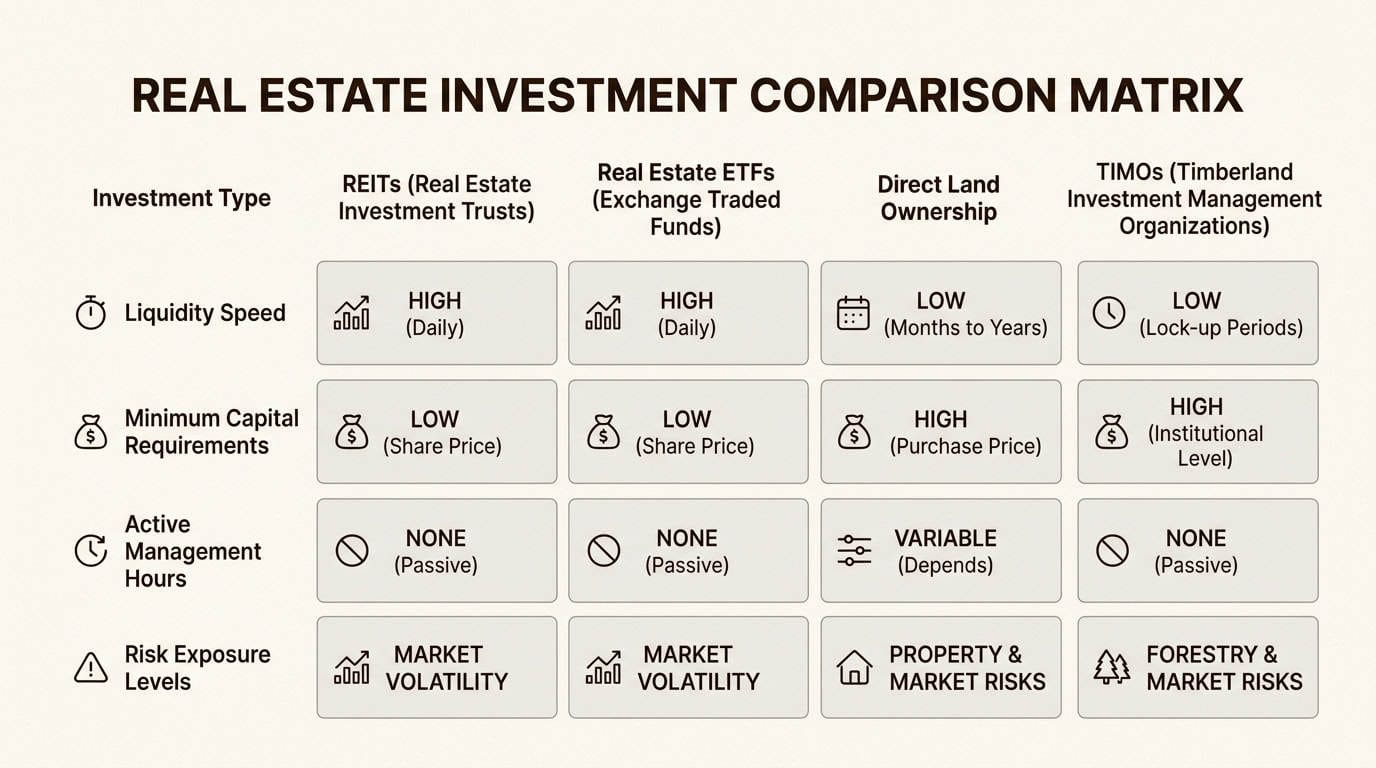

Method 1: Timberland REITs (Easiest, Most Liquid)

Real Estate Investment Trusts that own timberland are the simplest way to gain exposure. You buy shares through your brokerage account, collect dividends, and never have to worry about pine beetles or forest fires.

There are two major timberland REITs:

| REIT | Market Cap | Dividend Yield | Acres Owned | Ticker |

|---|---|---|---|---|

| Weyerhaeuser | $17.4B | 3.49% | 10 million | WY |

| Rayonier | $6.2B | 6.63% | 4.2 million | RYN |

Weyerhaeuser is the giant here. They own 10 million acres across the U.S. and manage Canadian timberlands under long-term licenses. They also operate 34 wood product manufacturing facilities, giving them vertical integration that smaller players lack. Their dividend policy is unique: a base quarterly payment plus variable supplemental dividends when lumber prices are high.

Rayonier recently merged with PotlatchDeltic in January 2026, creating a combined entity with 4.2 million acres across 11 states. The merger should allow them to ship over 1 billion board-feet of lumber in 2026. Their dividend yield is nearly double Weyerhaeuser’s, though this reflects a different capital allocation strategy rather than necessarily being “better.”

Pros: Liquid, dividend-paying, professional management, no expertise required

Cons: Interest rate sensitive (REITs borrow heavily), stock market correlation, no recreational use

Method 2: Timber ETFs (Diversified Exposure)

Exchange-traded funds offer exposure to the global timber industry without picking individual companies. Two options dominate:

- iShares Global Timber & Forestry ETF (WOOD)

- Invesco MSCI Global Timber ETF (CUT)

These funds hold baskets of timber companies worldwide, giving you geographic diversification. You’re not just betting on U.S. housing starts; you’re exposed to global timber demand including China (which has increased U.S. timber imports tenfold over the past seven years).

Pros: Instant diversification, low minimum investment, no management responsibilities

Cons: Less direct timber exposure, management fees, includes paper/packaging companies

Method 3: Direct Land Ownership (Full Control)

This is where timberland gets interesting. You buy the land. You own the trees. You make the decisions.

Minimum viable investment starts around 10 acres, though most serious timber operations are significantly larger. Land costs typically run $1,500 to $2,000 per acre, though this varies wildly by location, soil quality, and existing timber value.

Direct ownership gives you full control over harvest timing (crucial for maximizing returns), recreational use (hunting, hiking, camping), and potential land development upside. Many timberland tracts eventually become worth more as residential or commercial land than as working forest.

But let’s be honest about the downsides. Selling timberland takes 6 to 18 months. You’re dealing with illiquidity that makes real estate look like day trading. You need forestry expertise or the budget to hire a consulting forester. And when a hurricane hits or wildfires spread, you’re the one absorbing the loss.

Pros: Full control, recreational use, tax benefits, potential development upside

Cons: Illiquid, management intensive, requires expertise, concentrated risk

Method 4: TIMOs (For the Big Players)

Timber Investment Management Organizations are institutional-grade vehicles for serious capital. Think pension funds, university endowments, and family offices.

The four largest TIMOs (Hancock Timber Resource Group, Forestland Group, Campbell Global, and Resource Management Service) collectively manage over 15 million acres. Campbell Global alone, now part of J.P. Morgan Asset Management, oversees $9.1 billion in timber assets.

Minimum investments typically start around $30 million for individual accounts. Commingled funds (pooled investments) have lower thresholds but still require accredited investor status and substantial capital.

Pros: Professional management, institutional-grade deals, sophisticated strategies

Cons: High minimums, limited liquidity, restricted to wealthy investors

Method 5: Crowdfunding Platforms (Emerging Option)

A newer category of platforms is attempting to democratize timberland access. These operate similarly to real estate crowdfunding, allowing multiple investors to pool capital for specific timberland acquisitions.

This space is still evolving. Platforms come and go, fee structures vary widely, and track records are limited. For most investors, REITs or ETFs remain the more proven path.

Pros: Lower minimums than direct ownership, professional management

Cons: Emerging market risks, limited track records, platform risk

How Timberland Actually Makes You Money

Timberland generates returns through four distinct mechanisms. Understanding each helps explain why this asset class behaves differently than stocks or bonds.

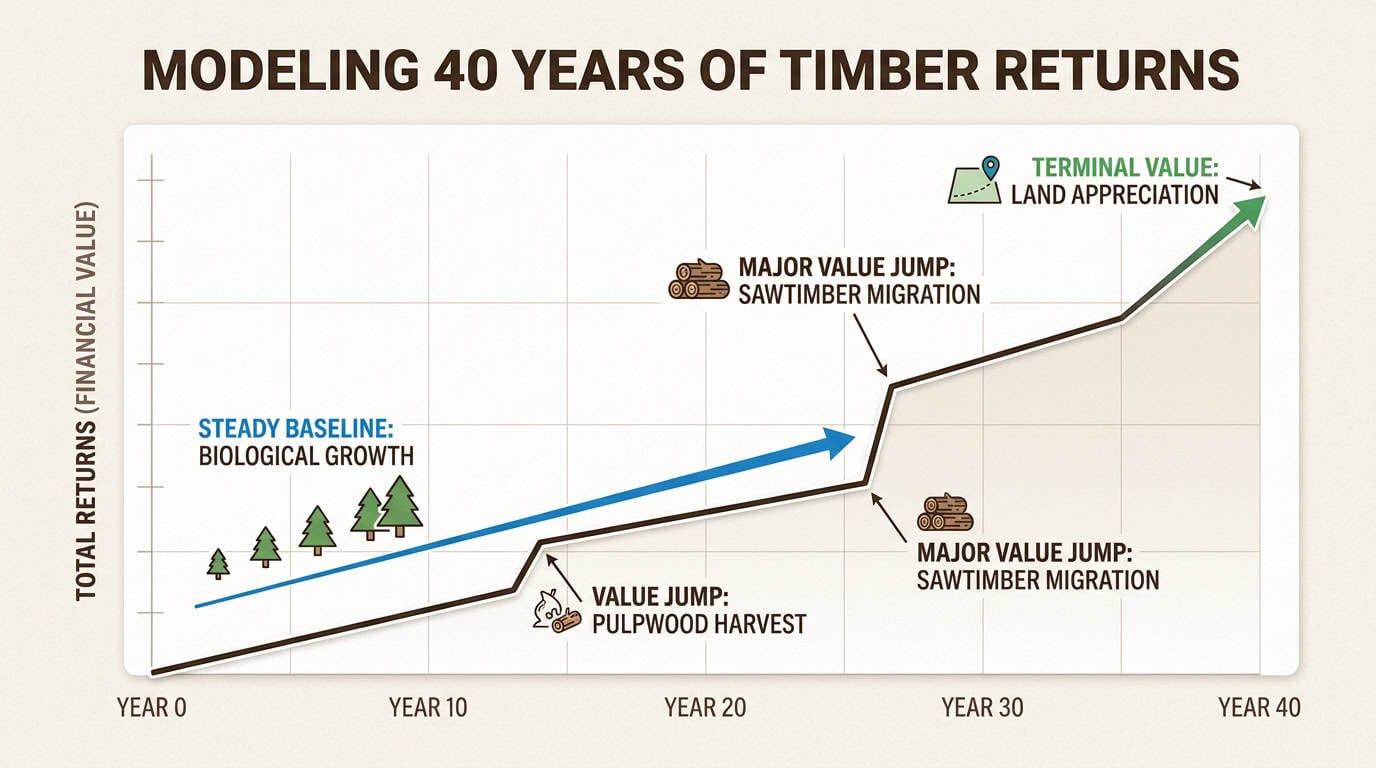

1. Biological Growth

Trees get bigger. It’s not complicated, but it’s powerful. A tree that adds 5% to its volume annually is effectively appreciating 5% per year, regardless of market conditions. This growth compounds over decades.

2. Product Class Migration

Here’s where timber gets interesting. Trees don’t just grow in volume; they grow into higher-value products:

| Tree Size | Product Class | Price per Ton | Example Value |

|---|---|---|---|

| 7″ diameter | Pulpwood | $7 | $1.50 per tree |

| 10″ diameter | Small sawtimber | $14 | $4.50 per tree |

| 14″ diameter | Large sawtimber | $30 | $22.50 per tree |

That 14-inch tree is worth 15 times the 7-inch tree, not because timber prices changed, but because the tree moved into a higher-value product category. This is unique to timberland. Your Apple stock doesn’t become a different, more valuable security just because you held it longer.

3. Land Appreciation

Land values typically contribute 5-7% of total timberland returns, but this can spike dramatically in growing regions. Timberland near expanding metropolitan areas sometimes gets rezoned for residential or commercial use, creating “higher and better use” scenarios where land value exceeds timber value.

4. Timber Price Cycles

Timber prices fluctuate with housing starts, construction activity, and global demand. The 2008 housing crash cut timber values roughly in half. Conversely, China’s surge in imports and Canada’s mountain pine beetle devastation (which reduced western Canadian timber volumes by over 50%) have supported U.S. prices.

Smart timberland owners time harvests to these cycles. Unlike stocks, you can “store” timber on the stump when prices are low and harvest when markets recover.

Alternative Income Streams

Beyond timber sales, landowners can generate revenue through:

- Hunting leases: $5-30 per acre annually depending on game quality

- Carbon credits: Emerging market for sequestered carbon

- Conservation easements: Tax incentives for preserving forestland

- Recreation permits: Camping, hiking, horseback riding access

The Brutal Truth: Risks Nobody Talks About

Timberland isn’t all peaceful walks through the forest and dividend checks. Let’s cover the risks that marketing materials conveniently omit.

Market Risks

Timber prices are cyclical and tied to housing starts. When construction slows, timber demand collapses. The 2008 financial crisis didn’t just hurt stocks; it devastated timber values. If you’re counting on steady timber income to fund retirement, you’re in for a rude awakening during housing downturns.

Environmental Risks

Nature doesn’t care about your investment timeline. Wildfires, hurricanes, ice storms, drought, insect infestations, and disease can destroy decades of growth in days. Canada’s mountain pine beetle epidemic wiped out more than half of western Canada’s timber volume. That devastation is permanent on human timescales; it takes 40-50 years to grow replacement timber.

Climate change is amplifying these risks. Drought stress makes trees more susceptible to pests. Warmer winters fail to kill off insect populations. Extreme weather events are becoming more common.

Liquidity Reality

You cannot sell timberland quickly. Six to eighteen months is typical for a sale. If you need cash for an emergency, medical expense, or better opportunity, your timberland is effectively frozen. This illiquidity premium is real, but so is the constraint on your financial flexibility.

Management Complexity

Direct timberland ownership requires expertise you probably don’t have. When do you thin? Which trees do you harvest? How do you negotiate with timber buyers? What’s a fair price for your stumpage?

Most direct owners hire consulting foresters (look for Association of Consulting Foresters members or Certified Foresters from the Society of American Foresters). This costs money but prevents costly mistakes. A poorly timed harvest or bad timber sale can cost you years of returns.

Interest Rate Sensitivity

Timberland REITs suffer when rates rise. Like all REITs, they use leverage to acquire properties. Rising rates increase borrowing costs and make their dividend yields less attractive compared to safer fixed-income alternatives. The past few years have demonstrated this dynamic clearly.

2026 Timberland Market Outlook

What’s ahead for timberland investors? The outlook is cautiously optimistic, with some important caveats.

Positive Drivers

Housing market recovery: After years of underbuilding, housing starts are climbing back toward historical norms. More construction means more lumber demand.

China exports: Chinese timber imports from the U.S. have increased tenfold over the past seven years. The Pacific Northwest has been the primary beneficiary, but demand ripples through North American markets.

Mass timber construction: A growing trend toward engineered wood products for commercial buildings is creating new demand categories. Mass timber (cross-laminated timber, glulam) is increasingly used for multi-story buildings, expanding timber demand beyond traditional framing lumber.

Carbon credit markets: While still emerging, carbon offset markets are creating potential new revenue streams for timberland owners who maintain standing forest. This is particularly relevant for institutional investors with ESG mandates.

Concerns

Recent price run-up: Timberland values have increased substantially due to low supply and capital seeking inflation hedges. This raises the risk of a market correction for new buyers entering at peak prices.

Interest rate environment: If rates remain elevated or climb higher, timberland REITs will face continued pressure. Their borrowing costs stay high and dividend yields look less attractive versus Treasuries.

Climate uncertainty: Increasing weather volatility creates unpredictable risks. One catastrophic wildfire season or hurricane can reshape regional timber markets.

Geographic Considerations

The U.S. South and Pacific Northwest remain the primary timberland investment regions. The South offers faster growth rates and lower land costs. The Pacific Northwest has older, more valuable timber and proximity to Asian export markets. Geographic diversification across both regions reduces concentration risk.

For ongoing market analysis, check our market commentary section.

Who Should (And Shouldn’t) Invest in Timberland

Timberland isn’t for everyone. Let’s be direct about who benefits and who should look elsewhere.

Good Fit For:

- Long-term investors: Timberland is a decades-long commitment, not a trade

- Diversification seekers: Low correlation to stocks and bonds reduces portfolio volatility

- Inflation hedgers: Historical positive correlation with inflation

- Hands-on owners: People who enjoy land management and outdoor recreation

- Wealth preservation: Families building multi-generational wealth

Bad Fit For:

- Short-term traders: You can’t flip timberland for quick profits

- Liquidity-dependent investors: If you might need the capital within 5-10 years, look elsewhere

- Passive investors: Direct ownership requires active management or oversight

- Small portfolios: With typical allocations of 5-10% for alternatives, you need substantial assets for direct ownership to make sense

Portfolio Allocation Guidance

Most financial advisors suggest limiting alternative investments (including timberland) to 5-10% of a portfolio. For a $500,000 portfolio, that’s $25,000-$50,000. At that level, timberland REITs or ETFs make sense. Direct land ownership typically requires a larger portfolio to achieve meaningful diversification.

For more on building a resilient portfolio, see our investor’s playbook.

Getting Started With Timberland Investing

If timberland investing fits your profile, here’s how to begin.

For Beginners: Start With REITs or ETFs

Buy shares of Weyerhaeuser or Rayonier through your existing brokerage account. Or purchase timber ETFs like WOOD or CUT. This gives you exposure without complexity. Monitor how these positions behave relative to your stocks and bonds. If you like the diversification benefits, consider expanding your allocation over time.

For Serious Investors: Research Direct Ownership

If you have the capital and expertise (or budget for professional management), direct ownership offers the highest potential returns and most control. Start by identifying target regions, understanding local timber markets, and connecting with consulting foresters. The Association of Consulting Foresters (ACF) and Society of American Foresters are good starting points for finding qualified professionals.

Key Resources

- NCREIF Timberland Index: Tracks institutional timberland returns

- ACF Foresters: Find qualified consulting foresters

- State forestry extension services: Free educational resources

- Local timber markets: Understand regional price dynamics

For additional investing guides and resources, explore our educational content.

The Bottom Line

Timberland investing offers something rare in modern finance: tangible assets that grow regardless of market sentiment. It’s not exciting, it’s not fast, and it’s not for everyone. But for patient investors seeking diversification, inflation protection, and the satisfaction of owning something real, timberland deserves consideration.

Start small if you’re curious. Learn the market dynamics. And remember: the best time to plant a tree was 20 years ago. The second best time is today.

Frequently Asked Questions

Is timberland investing 2026 a good strategy for beginners?

Beginners should start with timberland REITs or ETFs rather than direct ownership. These offer exposure to timber markets without requiring forestry expertise or large capital commitments. Once you understand how timber investments behave, you can consider direct ownership.

How much money do I need to start timberland investing 2026?

You can start with as little as $100 through timber ETFs. REITs require whatever your brokerage minimum is (often $0). Direct land ownership typically requires $50,000+ for a meaningful parcel, plus ongoing management costs.

What are the tax benefits of timberland investing 2026?

Timberland offers several tax advantages. Income from timber sales is typically treated as capital gains (lower rates than ordinary income). You can deduct property taxes, management expenses, and reforestation costs. Conservation easements may provide additional tax incentives. Always consult a tax professional for your specific situation.

How does timberland investing 2026 compare to stock market returns?

Historically, timberland returns have nearly matched the S&P 500 over long periods, but with roughly half the volatility. The NCREIF Timberland Index shows 20-year returns comparable to equities with risk levels closer to Treasury bonds.

What are the biggest risks in timberland investing 2026?

The major risks are market cyclicality (timber prices follow housing), environmental damage (wildfire, pests, weather), illiquidity (6-18 months to sell), and management complexity (requires expertise or professional help).

Can I lose money with timberland investing 2026?

Absolutely. Timberland is not risk-free. The 2008 housing crash cut timber values roughly in half. Poor management decisions, natural disasters, or buying at peak prices can all result in losses. Like any investment, due diligence matters.

Should I choose REITs or direct ownership for timberland investing 2026?

Choose REITs if you want liquidity, dividends, and professional management without the headaches. Choose direct ownership if you have substantial capital, want full control, can handle illiquidity, and enjoy land management. Most investors are better suited to REITs.

Keep Your Investing Skills Sharp

- Timber Stocks: The “Boring” Investment That Might Just Save Your Portfolio From Ruin

Discover why timber stocks quietly outperform flashy assets and how they can stabilize your portfolio when everything else is falling apart. - Raw Land Due Diligence: 7 Non-Negotiable Checks Before You Sign the Deed

Before you buy a single acre, learn the critical mistakes that can turn your “dream investment” into a financial sinkhole. - TradingView Review 2026: 7 Brutal Truths Traders Ignore

If you’re analyzing markets without the right tools, you’re guessing. Here’s how TradingView can sharpen your edge and keep emotion out of your decisions.