Emergency Cash Reserve: The 3-Tier System That Actually Works

The standard advice — “save 3 to 6 months of expenses” — is so vague it’s essentially useless. A real emergency cash reserve isn’t a single pile of money sitting in one account; it’s a layered system with three distinct tiers, each designed for a different threat level. I’ve spent 20 years learning this the hard way, and I’m handing you the shortcut.

At-a-Glance

| Tier | Coverage | Target Amount | Where to Keep It |

|---|---|---|---|

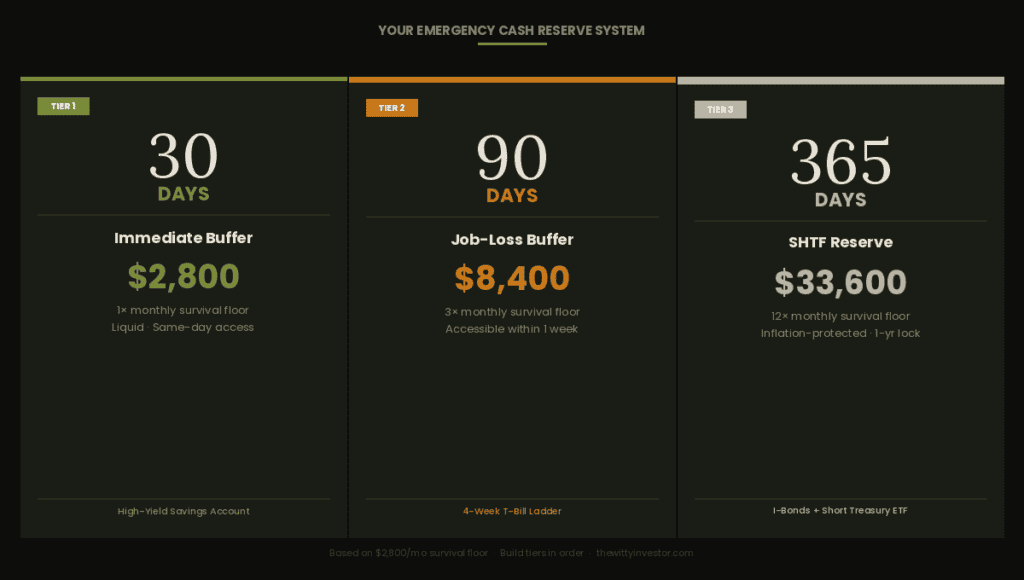

| Tier 1 | 30 days of survival floor | 1x monthly survival floor | High-yield savings account |

| Tier 2 | 90 days of survival floor | 3x monthly survival floor | T-bill ladder or money market |

| Tier 3 | 365 days of survival floor | 12x monthly survival floor | I-bonds + short Treasury ETF |

Survival floor = housing + utilities + groceries + transportation + minimum debt payments. Not your lifestyle number. Your “keep the lights on and the car moving” number.

Table of Contents

How Much Emergency Cash Reserve Do You Actually Need?

This is the question everyone asks and almost nobody answers properly. “Three to six months” is the financial equivalent of telling someone to dress “appropriately for the weather.” Technically true. Completely unhelpful.

I’ve had three separate moments in my financial life where I thought I had an adequate emergency cash reserve and discovered — mid-crisis — that I was wrong. The third one was bad enough that I stopped guessing and built an actual system.

Here’s what the standard advice gets wrong: it doesn’t distinguish between your lifestyle expenses and your survival floor. Your survival floor is what it costs you to not die financially — rent or mortgage, utilities, groceries, transportation to work, and minimum debt payments. Nothing else. No subscriptions, no dining out, no anything discretionary.

For most people, the survival floor runs 40–60% of normal monthly spending. Which means “3 months of expenses” at your lifestyle number could actually be 5–7 months of real survival runway. That’s useful information. But more importantly, it means you might be dramatically underbuilding your emergency cash reserve because you’re using the wrong denominator.

Calculate your survival floor first. Pull three months of bank and credit card statements, highlight only the essentials, and average the highlighted total. That number is the foundation of your entire emergency cash reserve framework. Everything else builds on it.

CFPB — How to build an emergency fund

The other thing the standard advice ignores: not all emergencies are the same size. A transmission replacement is not the same threat as a layoff. A layoff is not the same threat as a six-month medical leave. Treating every emergency as “draw from the same account” is how you drain your emergency cash reserve on a car repair and then face a job loss six weeks later with nothing left.

That’s why a single account doesn’t cut it. You need tiers.

The 3-Tier Emergency Cash Reserve System: Build It in Order

I’ve field-tested this framework through two decades of income disruptions, surprise bills, and one genuinely scary six-month period where I was very grateful I’d built this before I needed it. Think of it as your financial bug-out bag: three layers, three threat levels, three different storage locations.

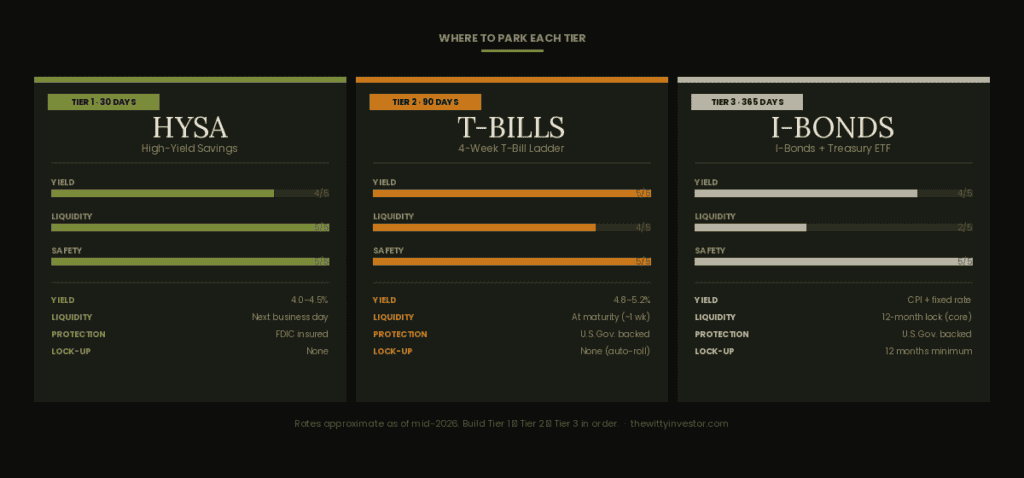

Tier 1 — The 30-Day Emergency Cash Reserve (Liquid, Zero Friction)

This is your first line of defense. Thirty days of survival floor expenses, sitting in a high-yield savings account at an online bank, accessible within one business day. Not I-bonds. Not a CD. Not your brokerage account. Boring, liquid cash.

Tier 1 handles: car repairs, appliance failures, medical copays, short income gaps, anything that used to go on a credit card. The whole point of this tier is that you can access it without friction, without penalty, and without selling anything.

Target: 1x your monthly survival floor. If your floor is $2,800/month, Tier 1 is $2,800.

The account matters. I keep my Tier 1 emergency cash reserve at an online bank that is not linked to my debit card. The extra 48-hour psychological friction of needing to transfer it before I can spend it has saved me from more bad decisions than I’d like to admit. Bankrate HYSA rate comparison keeps current rate data — you want north of 4% APY right now. Any brick-and-mortar savings account paying 0.01% is actively shrinking your reserve in real terms.

High-yield savings account — open one here

Tier 2 — The 90-Day Emergency Cash Reserve (Accessible, Earning)

This is your job-loss buffer. Three months of survival floor expenses, held in something slightly less instant than a HYSA but still accessible within a week.

| Vehicle | Liquidity | Approx. Yield | Notes |

|---|---|---|---|

| High-Yield Savings | 1 business day | 4.0–4.5% APY | Simplest; FDIC insured |

| Money Market Fund | 1–2 business days | 4.5–5.0% | Higher yield; not FDIC |

| 4-Week T-Bill Ladder | At maturity (~weekly) | 4.8–5.2% | Auto-rollable; state-tax exempt |

| 3-Month CD | At maturity | 4.5–5.0% | Early withdrawal penalty applies |

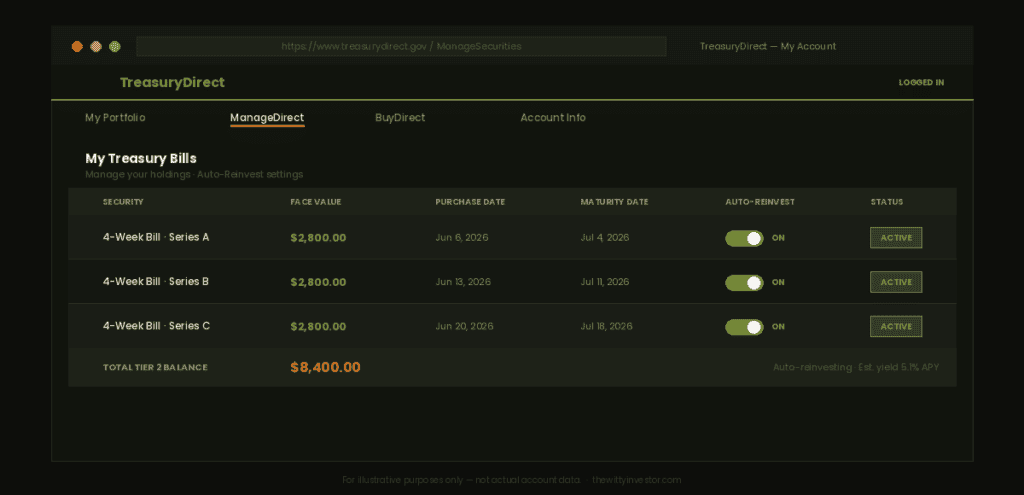

I run my Tier 2 emergency cash reserve as a rolling 4-week T-bill ladder through TreasuryDirect.gov. You buy a 4-week bill, set it to auto-reinvest, and it rolls every month. If you need the money, you stop the reinvestment and have cash within a week. The state income tax exemption on T-bill interest is a real bonus if you’re in a high-tax state — it can add 0.3–0.5% to your effective yield without changing anything.

Target: 3x your monthly survival floor. In our $2,800 example, that’s $8,400.

Tier 3 — The 365-Day Emergency Cash Reserve (Preserved, Inflation-Protected)

This is the SHTF tier. A full year of survival floor expenses in assets that preserve purchasing power over a 12–24 month horizon.

Most people never build Tier 3. They stop at Tier 2 and call it done. That’s fine for routine disruptions. But Tier 3 is insurance against scenarios where Tier 1 and Tier 2 both run dry before the situation resolves — extended medical leave, industry-wide layoffs, prolonged economic disruption. If you’ve ever thought “I could lose this job and not be able to find another one for a year,” you need Tier 3.

TreasuryDirect.gov — I-bond information

I split my Tier 3 emergency cash reserve between I-bonds (for the inflation protection and government backing) and a short-term Treasury ETF (for the liquidity margin). The I-bonds have a 12-month lock-up, which is actually a feature at this tier — it creates enough friction that you won’t raid your long-term reserve for a short-term problem.

Target: 12x your monthly survival floor. Yes, that’s $33,600 in our example. No, you don’t build it all at once. You build the tiers in order, over time, like stacking canned goods in a prepper pantry — systematically, without rushing, until the shelf is full.

Best Accounts to Park Your Emergency Cash Reserve (By Tier)

Before the good options, a quick word on bad ones.

Do not keep your emergency cash reserve in:

- Your primary checking account (you will spend it without noticing)

- A brokerage investment account (market risk means it drops when you need it most; settlement takes 2+ days)

- Whole life insurance cash value (illiquid, expensive to access, sold to you by someone who earned a commission)

- A CD without understanding the early withdrawal penalty

Tier 1 — Best HYSA Options

Look for: no minimum balance, no monthly fees, APY consistently above 4%, same-day or next-day transfer to your primary bank. The specific bank matters less than the rate and the separation from your spending account.

Tier 2 — T-Bills vs. Money Market

If you want simplicity, a money market fund at a major brokerage works. Fidelity’s SPAXX and Vanguard’s VMFXX both currently yield in the 4.5–5% range.

Fidelity money market fund overview

If you want to optimize, the 4-week T-bill ladder via TreasuryDirect edges both of those on an after-tax basis in most states. Takes about 20 minutes to set up, then runs on autopilot.

Tier 3 — I-Bonds + Short Treasury ETF

I-bonds through TreasuryDirect for the core inflation-protected position (maximum $10,000/year per person). For additional Tier 3 emergency cash reserve capacity beyond $10K, a short-term Treasury ETF Bogleheads wiki on bond funds gives you liquidity without meaningful credit risk.

Compile: Calculating Your Emergency Cash Reserve Numbers

Two numbers. That’s all you need to get started.

Number 1: Your survival floor. Pull three months of statements. Highlight housing, utilities, groceries, transportation, minimum debt payments. Average the highlighted total. Write it down.

Number 2: Your current gap. Total your accessible non-investment cash. Subtract from your Tier 1 target. That’s the immediate number you’re working toward.

If that gap number is uncomfortable, good. Discomfort is information. I’ve stared at that number in some dark financial moments and it’s always better to know than to not know.

Debug: Emergency Cash Reserve Mistakes I’ve Made So You Don’t Have To

Counting retirement accounts as part of my emergency cash reserve. They’re not. A 401(k) early withdrawal costs 10% penalty plus ordinary income tax. In a 24% bracket, you’re surrendering 34 cents of every emergency dollar just to access your own money. That is not a reserve. That is an expensive last resort.

Building Tier 3 before Tier 1 was funded. I was excited about I-bonds and jumped ahead. Then my car’s engine died. My “savings” were locked up for 12 months. The repair went on a credit card. The interest I paid on that card wiped out months of I-bond gains. Build in order.

Using my lifestyle spend instead of my survival floor. Made my emergency cash reserve feel adequately funded when it wasn’t. Running the survival floor calculation changed my target by about 40%. That 40% gap could have been catastrophic in a real extended emergency.

Investopedia — common emergency fund mistakes

Treating it as an investment. The emergency cash reserve is not an optimization problem. It’s insurance. The moment I started chasing yield across too many accounts, I lost track of what I had and where it was. Boring and organized beats clever and scattered every time.

Stack: A Realistic Build Timeline

Starting from $500 in savings, building at $400/month:

| Month | Action | Tier 1 Balance | Tier 2 Balance |

|---|---|---|---|

| 1–2 | Open HYSA, automate $400/mo | $800 | — |

| 3–7 | Continue contributions | $2,800 | — |

| 7–8 | Tier 1 complete; open T-bill account; redirect $400/mo | $2,800 | $800 |

| 9–24 | $400/mo into T-bill ladder | $2,800 | $8,400 |

| 25+ | Tier 2 complete; begin Tier 3 (I-bonds) | $2,800 | $8,400 |

Eighteen months to Tier 2. Two years to start stacking Tier 3. That’s a manageable timeline — it just requires automating the transfer and not touching it.

Deploy: When and How to Actually Use Your Emergency Cash Reserve

The reserve only works if you use it correctly.

- Always hit Tier 1 first. Don’t pull from Tier 2 for a $400 repair when Tier 1 exists for exactly that purpose.

- Replenish immediately. The moment the emergency passes, go back to funding the depleted tier before moving up the stack.

- Defend the definition. A vacation deal is not an emergency. A flight to a wedding is not an emergency. A busted water heater is an emergency. Defend the boundary or the whole system collapses.

The prepper analogy holds: you don’t crack your 90-day food supply because you’re too tired to go grocery shopping. The reserve exists for actual threats — not inconveniences you could have planned for.

FAQ

How much should my emergency cash reserve be? Minimum: 30 days of your survival floor (Tier 1). Realistically: 90 days accessible within a week (Tier 2). Ideally: 365 days in a slightly less liquid vehicle (Tier 3). Calculate your survival floor first — it’s typically 40–60% of your normal monthly spend and will be lower than you expect.

Is a high-yield savings account enough for an emergency cash reserve? For Tier 1, yes — it’s the ideal vehicle. For Tier 2, you can do better on yield with T-bills or a money market fund. For Tier 3, you want inflation protection that a HYSA doesn’t provide.

Can I use my Roth IRA contributions as an emergency cash reserve? Technically you can withdraw Roth contributions (not earnings) penalty-free. But I strongly advise against treating your Roth as an emergency fund — the compounding you sacrifice by pulling money out early is significant, and it trains you to see retirement accounts as accessible. Build a real emergency cash reserve instead.

What’s the difference between an emergency fund and an emergency cash reserve? Same concept, better framing. “Emergency cash reserve” emphasizes that it’s cash (liquid, accessible) and reserved (not for general spending). The distinction matters practically: it helps you resist putting the money somewhere with higher returns but lower liquidity.

Should I pay off debt or build an emergency cash reserve first? Build Tier 1 first, always. Without a 30-day emergency cash reserve, every unexpected expense goes on a credit card and erases your debt payoff progress. Once Tier 1 is funded, pivot aggressively to high-interest debt. Build Tier 2 after the expensive debt is gone.

What actually qualifies as an emergency? Job loss, medical expense beyond your HSA/insurance coverage, essential vehicle repair (you need it to work), essential home repair (structural, plumbing, heating), emergency travel for a family crisis. Not: sales, experiences, non-essential purchases, or anything you could have anticipated and saved for separately.

How do I know when to use Tier 2 vs. Tier 1? Tier 1 for anything under 30 days of coverage and fully resolvable in the short term. Tier 2 when you’re facing an extended disruption (job loss, prolonged illness) that will last beyond what Tier 1 can cover. The tiers are sequential — deplete lower tiers before touching higher ones.

How often should I recalculate my emergency cash reserve target? Any time your survival floor changes meaningfully: new housing costs, new debt obligations, income change, new dependents. Otherwise, an annual check is sufficient.

Continue Building Your Financial Foundation

Ultimate Guide to Timberland Investing in 2026: 5 Ways to Own Trees

Looking for a hedge against inflation that goes beyond traditional stocks and bonds? Learn how timberland investing works, the different ways to gain exposure, and why trees have quietly become one of the market’s most resilient long-term assets.

Prepper Stocks 2025: Profit from the Survival Industry Before It Goes Full Mad Max

If you think preparedness is becoming big business, you’re not wrong. Take a look at the companies benefiting from growing demand for survival gear, emergency supplies, outdoor equipment, and self-reliance as more Americans prepare for uncertain times.

Dividend Defense: Stocks That Survive Market Chaos in 2026

Once your cash reserves are in place, it’s time to put your money to work. Discover dividend-paying companies that have historically weathered recessions, inflation, and market volatility better than most.