M1 Finance vs. TradingView: A Cynical Strategist’s Real Verdict After 20 Years in the Market

M1 Finance vs. TradingView isn’t actually a fight — it’s a mismatched pairing dressed up as a rivalry by SEO listicles that have never placed a real trade. M1 Finance is the autopilot that buys, rebalances, and reinvests while you go live your life; TradingView is the instrument panel you use to decide what deserves a seat in that portfolio in the first place. I’ve spent two decades watching otherwise smart people misunderstand exactly this distinction, and it has cost them real money — so let’s fix that before you make the same mistake.

At-a-Glance: The M1 Finance vs. TradingView Verdict

| Tool | My Call | Why |

|---|---|---|

| M1 Finance | BUY | Best-in-class for automated, long-term portfolio management |

| TradingView | HOLD | Excellent research and charting, but it isn’t a brokerage — don’t mistake it for one |

| M1 Finance vs. TradingView, used together | BUY | This is the combination most investors actually need |

| Picking only one and ignoring the other | AVOID | You’re solving half the problem and calling it a strategy |

I’ve been doing this — analyzing markets, managing my own money, and watching other people manage theirs badly — for more than 20 years now. I was around for the 2008 financial crisis when the Dow lost more than half its value and otherwise rational adults sold everything at the exact bottom because their lizard brains overruled their financial plan.

I was around in 2021 when speculative tech names, SPACs, and meme stocks turned every group chat into a hedge fund and most of those gains evaporated within twelve months. So when I tell you that the real risk in the M1 Finance vs. TradingView debate isn’t picking the “wrong” platform — it’s letting the wrong platform encourage the wrong behavior — I’m not theorizing. I watched it happen to people with engineering degrees who should have known better.

Table of Contents

What Is M1 Finance vs. TradingView, Really? (Cutting Through the Marketing Copy)

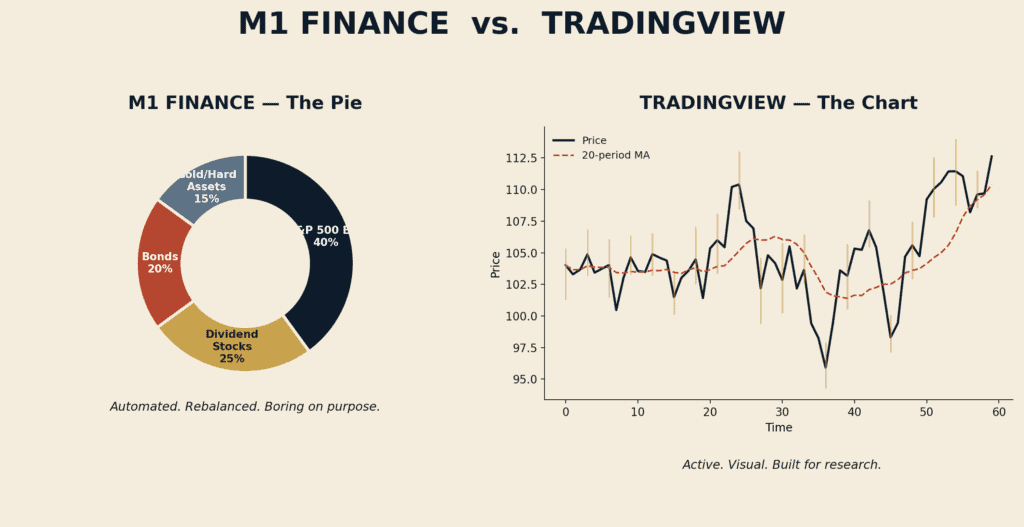

Let’s strip the buzzwords. M1 Finance is a registered brokerage. It holds your money, executes your trades, and — this is the part people miss — automatically rebalances your portfolio based on percentage targets you set once and barely have to touch again. You build a “pie,” assign weights to ETFs and individual stocks, and every dollar you add gets routed to whatever slice is underweight.

It’s the closest thing retail investing has to a crockpot: load it, walk away, come back to something that actually turned out fine. NerdWallet’s 2026 review of M1 Finance points out it’s a genuinely niche product — the trading platform and research tools score lower than full-service brokers, but for investors who already know what they want to own and just need the system to maintain it, that’s beside the point.

TradingView, on the other hand, holds none of your money. It’s a charting and analysis platform — arguably the best one retail traders have ever had access to, with hundreds of built-in indicators, a scripting language (Pine Script) for building your own, and a social network of traders publishing their ideas in public. StockBrokers.com’s TradingView review calls it one of the most widely used charting platforms in the world for good reason — but it also notes the charting tools can overwhelm beginners who wander in without a plan.

That’s the crux of the M1 Finance vs. TradingView confusion: one is a wealth-building engine, the other is a magnifying glass. Conflating the two is how people end up day-trading their retirement account or, worse, never investing at all because they think research is the same thing as ownership.

My 20 Years of Watching Investors Misuse Both Tools

Here’s the uncomfortable truth nobody selling you a platform will say out loud: the tool was never the problem. I’ve watched disciplined investors build wealth slowly and boringly with both M1 Finance and TradingView in their toolkit, and I’ve watched undisciplined investors torch capital using either one in isolation. The M1 Finance vs. TradingView decision matters less than most financial influencers pretend, because the bigger variable is always the person holding the mouse.

M1 Finance vs. TradingView for Long-Term Dividend Investors

If your goal is compounding dividends and letting time do the heavy lifting, the M1 Finance vs. TradingView calculus tilts hard toward M1. Dividend reinvestment, automated rebalancing back to target weights, and the ability to mix broad index ETFs with individual dividend payers inside one “pie” is exactly the kind of boring, repeatable mechanism that long-term compounding rewards.

TradingView still earns a supporting role here — I use it to screen for dividend sustainability before a stock ever earns a slice in my pie — but it’s a pre-purchase tool, not a holding mechanism. I learned this lesson the hard way: in the run-up to 2008, I was anchored to the idea that a few “safe” dividend names couldn’t fall apart, and I didn’t rebalance fast enough when their payout ratios started flashing warning signs. Automated rebalancing, the kind M1 Finance specializes in, would have forced the discipline my emotions weren’t providing.

The Behavioral Finance Problem Nobody Talks About

Here’s where I get cynical, because somebody has to be. The financial industry sells products, not psychology, and psychology is the actual battlefield. The M1 Finance vs. TradingView question isn’t really “which platform has better features” — it’s “which platform exposes me to which cognitive traps.”

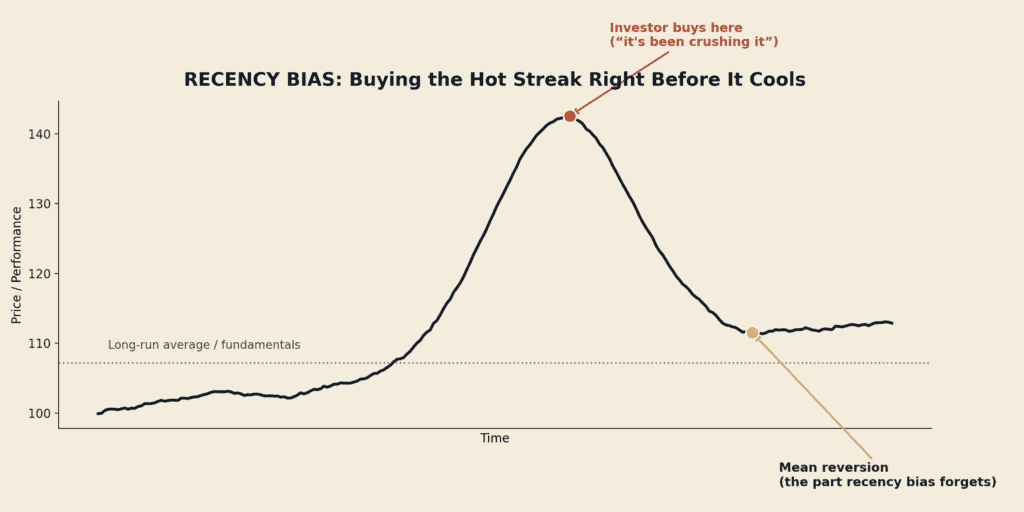

TradingView’s real-time charts and social feed are a recency bias machine. Morningstar’s research on recency bias found that investors who bought based on recent outperformance systematically underperformed afterward — and a platform built around constant, beautifully rendered, real-time price action is the perfect delivery mechanism for that exact mistake. M1 Finance has the opposite problem: its limited trading windows and “pie” structure are designed to bore you into good behavior, which is a feature right up until you need to make a genuinely important change and the system makes you wait.

M1 Finance vs. TradingView for Swing Trading and Active Traders

If you’re an active trader — someone with real opinions about next week’s price action, not just next decade’s — the M1 Finance vs. TradingView comparison flips entirely. TradingView is built for this. Its alert system, screener, and Pine Script backtesting exist specifically to let you test a thesis before risking capital on it. M1 Finance, by design, will frustrate an active trader: there’s no options trading, limited trading windows, and a structure that actively discourages the kind of frequent repositioning that swing trading requires.

I’m not anti-trading — some of my best years came from disciplined, rules-based short-term positions — but I’m allergic to people pretending M1 Finance is a trading platform. It isn’t trying to be one, and that’s by design, not a flaw.

Side-by-Side: The Cold, Hard Comparison Tables

I promised data, not vibes. Here’s how the platforms stack up on mechanics:

| Feature | M1 Finance | TradingView |

|---|---|---|

| Holds your money | Yes (registered brokerage) | No (charting/analysis only) |

| Automated rebalancing | Yes | No |

| Charting depth | Basic | Best-in-class, 100+ indicators |

| Custom scripting | No | Yes (Pine Script) |

| Options trading | No | Via connected broker only |

| Social/community features | Minimal | Extensive |

| Built for | Buy-and-hold, automated investing | Active research, technical analysis |

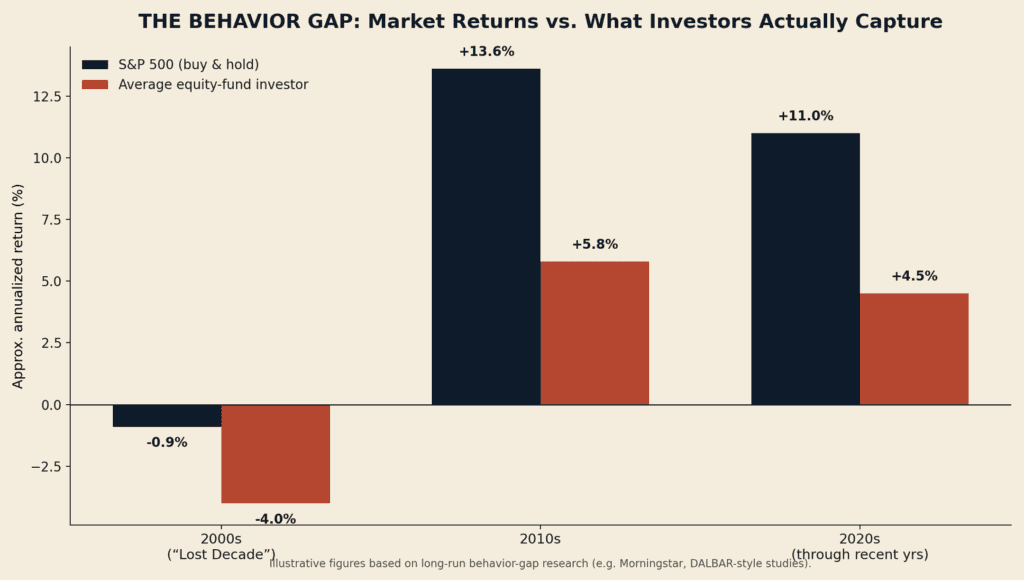

And because the M1 Finance vs. TradingView debate ultimately comes down to investor behavior, not platform mechanics, here’s a table that should scare you a little more than the feature comparison does — the actual gap between market returns and investor returns over time, driven almost entirely by the behaviors a platform either encourages or discourages:

| Period | S&P 500 Annualized Return | Average Equity Fund Investor Return (behavior gap) |

|---|---|---|

| 2000s (“Lost Decade”) | Roughly flat | Negative, due to buying high and selling low |

| 2010s | Double-digit annualized | Meaningfully lower, due to under-investment during volatility |

| 2020s (through recent years) | Strong but volatile | Lower still, with sharp underperformance around 2021–2022 |

That gap is the entire reason the M1 Finance vs. TradingView decision has psychological stakes, not just technical ones. The market doesn’t punish you for using the wrong app. It punishes you for letting either app talk you out of your own plan.

One more table, because valuations and dividend metrics matter more than people pretend during a panic. After the 2008 crash, defensive names like Walmart traded at modest multiples with healthy yields — conditions that don’t exist after over a decade of multiple expansion, as The Motley Fool’s retrospective notes:

| Metric | “Defensive” Stock, Post-2008 | Same Profile Today |

|---|---|---|

| P/E ratio | Roughly mid-teens | Often double that or higher |

| Dividend yield | Comparable to broad market | Often well below broad market |

| Payout ratio | Conservative | Tighter, less room for error |

That’s not a stock pick — it’s a warning about anchoring to “what worked last time,” which brings us right back to behavioral finance.

Lessons From 2008 and the 2021 Bubble I’d Rather Not Repeat

I owned shares in companies that nearly didn’t survive 2008. I didn’t panic-sell, mostly because I’d built a system that made panic-selling annoying rather than easy — which is, not coincidentally, exactly what M1 Finance’s automated structure does today for people who didn’t live through that crash personally. The Motley Fool’s retrospective on financial-crisis lessons makes the same point I make to anyone who’ll listen: panic-selling, not the crash itself, is usually what destroys long-term returns, because investors who sell during the trough rarely buy back in before the recovery is well underway.

Then came 2021, and a different flavor of the same disease. Cheap money and a culture of screenshotting gains on social platforms turned speculation into entertainment. TradingView’s social feed — to be clear, a genuinely useful research tool when used with discipline — became, for plenty of less experienced traders, a highlight reel of survivorship bias. You don’t see the accounts that blew up; you see the one chart that 10x’d. That’s not a flaw unique to TradingView. It’s a flaw in human psychology that any charting and social platform will amplify if you let it.

Is M1 Finance vs. TradingView the Right Combo for Beginner Investors?

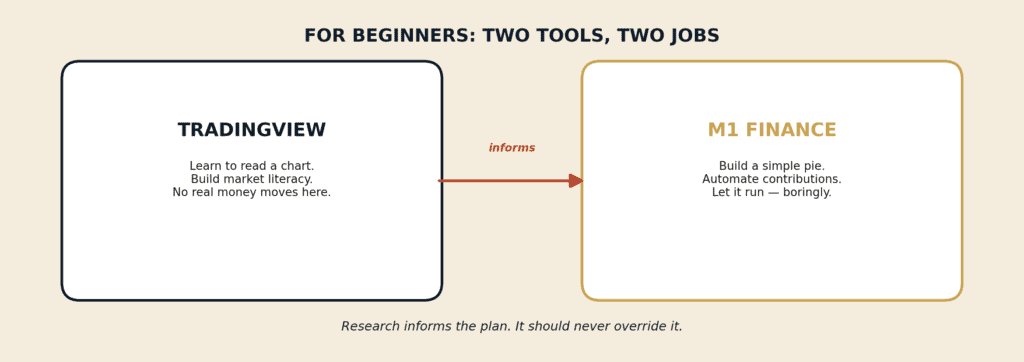

For most people just getting started, the M1 Finance vs. TradingView answer is “use both, but understand your job in each one.” Open an M1 Finance account, build a simple pie of low-cost index ETFs, automate your contributions, and let it run. Open a free TradingView account separately to learn how to read a chart, understand basic concepts like the Relative Strength Index, and build market literacy — not to time entries into your retirement account.

The single biggest mistake I see beginners make in the M1 Finance vs. TradingView decision isn’t choosing the “wrong” one. It’s importing TradingView’s trading mentality into an M1 Finance account that was never designed to be actively managed, and then panicking when normal volatility looks like a five-alarm fire on a real-time chart.

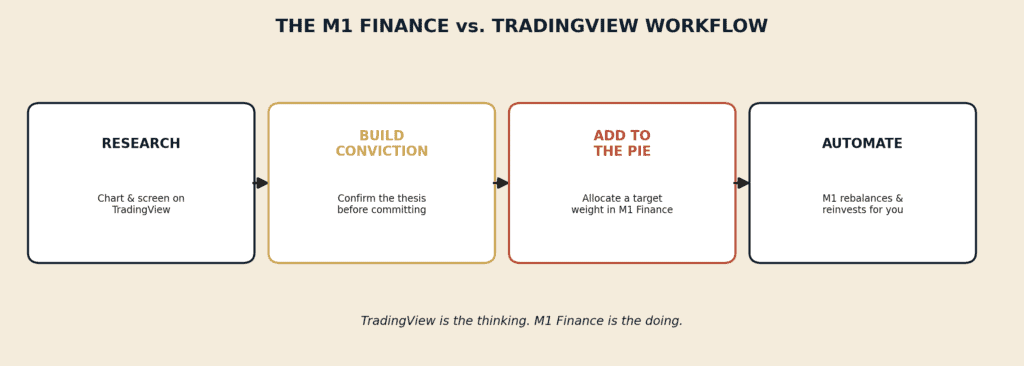

How I’d Actually Use Both (My Personal Setup)

After 20-plus years, here’s the unglamorous truth about how I run things: the bulk of my long-term capital sits in an automated, rebalanced structure that looks a lot like an M1 Finance pie — boring on purpose, because boring compounds. A smaller, clearly bounded portion of capital is allocated to positions I research using charting tools in the TradingView style, with rules about position sizing and exit points decided before I open the chart, not while I’m staring at it.

The M1 Finance vs. TradingView split in my own portfolio is roughly proportional to how much of my financial future I’m willing to leave to active judgment versus systematic discipline — and the honest answer, after watching 2008 and 2021 up close, is that I trust the system more than I trust my own real-time impulses.

The Verdict

If you force me to pick a single winner in the M1 Finance vs. TradingView matchup, I’ll refuse, because the question is a trap dressed up as a comparison. M1 Finance wins for anyone who wants to build wealth automatically without babysitting a portfolio — it’s a brokerage built around behavioral discipline, and that discipline is worth more than any feature list.

TradingView wins for anyone who wants to understand markets deeply, build a research process, and develop genuine market literacy — but it will not manage a single dollar for you, and pretending otherwise is how good research turns into bad trading.

The real winner of the M1 Finance vs. TradingView contest, for most people reading this, is the combination: research on one, automation on the other, and a firewall between the two so that real-time price anxiety never gets to override a long-term plan.

FAQ: M1 Finance vs. TradingView and the Psychological Traps That Get Investors

Is M1 Finance or TradingView better for beginners? Neither is “better” in isolation — M1 Finance is better for actually owning and managing investments as a beginner; TradingView is better for learning to read markets. The trap is using TradingView’s intensity to manage decisions inside an M1 Finance account meant for the long haul.

Can I lose money just from watching charts too much? Indirectly, yes. Watching real-time price movement on a platform like TradingView while holding long-term positions tends to trigger loss aversion and recency bias — a well-documented cognitive bias where the pain of a paper loss feels roughly twice as intense as an equivalent gain — which pushes people toward selling at exactly the wrong moment.

What is anchoring bias, and how does it show up in the M1 Finance vs. TradingView decision? Anchoring bias is the tendency to fixate on an initial reference point — your purchase price, a past high — even after new information should change your view. It shows up constantly on charting platforms, where a prior high or round-number price level can irrationally dictate buy and sell decisions long after the fundamentals have shifted.

Is dollar-cost averaging better done through M1 Finance or TradingView? M1 Finance, without question. Dollar-cost averaging is a mechanical, scheduled investing strategy, and TradingView doesn’t execute trades or hold assets — it’s a research tool. M1 Finance’s automated recurring investments are built precisely for this.

Should I avoid TradingView entirely if I’m a long-term investor? No — that overcorrects. Used as a research and literacy tool with firm boundaries (no checking it daily, no impulse trades), TradingView can sharpen your understanding of the names you hold inside M1 Finance. The danger isn’t the tool; it’s unlimited access without a rule book. This is the M1 Finance vs. TradingView nuance most beginners skip past on their way to picking a side.

What’s the single biggest behavioral trap in the M1 Finance vs. TradingView debate? Mistaking information for action. TradingView gives you more information than almost any retail platform in existence. M1 Finance gives you a system that doesn’t need your daily input to work. The trap is assuming more information should translate into more activity — when, for most long-term investors, the opposite is true.

Keep Reading (Before You Go Blow Your Budget on Something Dumb)

👉 What Does Palantir Do? (And Should You Actually Invest in It?) Now that you understand financial basics, here’s how to apply them to a real company without getting lost in buzzwords and hype.

👉 M1 Finance News 2026: Key Updates, Rate Changes, and What Investors Should Watch Because your platform matters. Here’s what M1 is changing, what it means for your money, and whether it’s helping you build wealth… or just rearranging the furniture.

👉 7 Tools I Use to Analyze Stocks Faster (and Smarter) If you’re ready to move from “I should invest” to “I actually know what I’m doing,” start here.